Navigating Agricultural Markets Amid U.S. Trade Policy Uncertainty: A Geopolitical Risk Playbook – AInvest

Report on U.S. Agricultural Trade Dynamics and Their Implications for Sustainable Development Goals

Executive Summary

The United States is projected to face a record agricultural trade deficit of $49.5 billion in Fiscal Year 2025. This development, driven by geopolitical tensions and protectionist trade policies, poses significant challenges to global food systems and the achievement of the United Nations Sustainable Development Goals (SDGs). This report analyzes the current trade landscape, outlines investment strategies aligned with sustainable development, and provides recommendations for navigating market volatility while contributing to global resilience.

Geopolitical Headwinds and Their Impact on Sustainable Development

Trade Policies as a Barrier to SDG 2 (Zero Hunger)

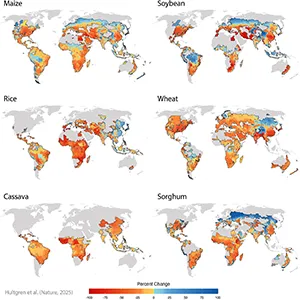

Current geopolitical friction directly undermines global efforts to achieve Zero Hunger (SDG 2). Retaliatory tariffs, including China’s 50% duties on U.S. soybeans and the European Union’s restrictions on U.S. beef, disrupt established food supply chains, impacting food availability and price stability. The resulting shift in trade flows has seen Brazil and Argentina increase their share of China’s soybean imports to 60%, up from 40% in 2022. This volatility creates uncertainty for producers and consumers alike, threatening the stability of the global food supply and hindering progress toward ensuring access to safe, nutritious, and sufficient food for all.

Erosion of SDG 17 (Partnerships for the Goals)

The escalating trade disputes represent a significant setback for global cooperation, a cornerstone of SDG 17. The prospect of renewed “reciprocal tariffs” by the U.S. administration in August 2025 further jeopardizes international partnerships. Such unilateral actions weaken the multilateral trading system, making it more difficult to address complex global challenges like climate change, poverty, and food insecurity through collaborative action.

Investment Strategies for Resilient Food Systems and Sustainable Growth

Aligning Investment with SDG 12 (Responsible Consumption and Production)

Investors can navigate this complex environment by adopting strategies that not only mitigate risk but also promote the development of more resilient and sustainable food systems, in line with SDG 12. A strategic approach involves the following:

- Hedging for Economic Stability (SDG 8): Allocating capital to diversified agricultural Exchange-Traded Funds (ETFs), such as the WisdomTree Broad Commodities (PCOM), can protect portfolios from volatility. This strategy supports market stability, which is essential for sustaining economic growth and decent work in the agricultural sector (SDG 8).

- Geographic Diversification for Global Food Security (SDG 2 & 17): Reducing dependency on U.S.-centric assets by investing in global agribusiness leaders like Brazil’s JBS and BRF supports a more distributed and resilient global food supply. Furthermore, emerging trade corridors, such as the U.S.-U.K. partnership, offer opportunities to foster new alliances for sustainable trade, provided they adhere to high environmental and food safety standards.

- Localizing Supply Chains for Resilience (SDG 12): Investing in companies that are localizing their supply chains, such as Tyson Foods’ expansion of domestic processing, helps insulate operations from international trade disruptions. This approach can reduce transportation-related carbon emissions and strengthen local economies, directly contributing to more sustainable production patterns.

- Monitoring Commodity Volatility for Market Efficiency: Extreme price fluctuations, such as the 100% surge in cocoa prices in 2024, highlight supply chain vulnerabilities. While investors can utilize instruments like the iPath Bloomberg Cocoa Subindex Total Return (NIB) to engage with this volatility, it underscores the urgent need for more stable and predictable production systems.

Opportunities and Systemic Risks in the Pursuit of Food Security

Advancing SDG 2 Through Infrastructure Investment

A heightened global focus on food security is creating investment opportunities that align directly with SDG 2. Government initiatives, such as China’s increased budget for stockpiles and India’s maintenance of large rice reserves, signal a long-term demand for advanced agricultural storage and logistics infrastructure. Investments in these areas can enhance the efficiency and resilience of food distribution networks.

Risks to Sustainable and Equitable Development

- Market Distortions and Inequality (SDG 10): Aggressive stockpiling by major economies risks creating market distortions that could lead to sudden price collapses, disproportionately harming agricultural producers in smaller, developing nations and exacerbating inequalities.

- Regulatory Hurdles to Collaboration (SDG 16 & 17): Increased regulatory scrutiny over cross-border mergers, such as the Bunge-Viterra acquisition, can impede the formation of strong global partnerships and institutions needed to manage strategic food assets effectively.

- Policy Instability (SDG 16): Ongoing legal challenges to trade tariffs underscore the unpredictability of the current policy environment, undermining the stable and just institutional frameworks required for sustainable long-term investment.

Concluding Recommendations for Sustainable Agricultural Investment

- Allocate 5–10% of portfolios to diversified agricultural ETFs to hedge against market shocks that threaten progress on SDG 2 (Zero Hunger) and SDG 8 (Decent Work and Economic Growth).

- Invest in globally diversified agribusinesses that are building resilient supply chains and fostering international partnerships, thereby advancing SDG 17 and SDG 12.

- Avoid overexposure to sectors highly sensitive to tariffs, such as U.S. soybeans and corn, until there is a clear resolution to trade disputes that undermine global cooperation.

- Maintain vigilant monitoring of the geopolitical landscape, particularly U.S.-China relations, to navigate risks to the stable institutions (SDG 16) necessary for achieving the 2030 Agenda for Sustainable Development.

1. Which SDGs are addressed or connected to the issues highlighted in the article?

SDG 2: Zero Hunger

- The article’s core subject is agricultural commodities such as soybeans, beef, grains, livestock, cocoa, rice, and wheat. It discusses issues of “food security,” supply chain disruptions, and stockpiling, all of which are central to ensuring access to food and ending hunger.

SDG 17: Partnerships for the Goals

- The text extensively covers international trade dynamics, including “trade disputes,” “retaliatory tariffs,” “trade deals” (U.S.-U.K.), and “geopolitical tension.” These elements directly relate to the goal of fostering a global partnership for sustainable development, particularly concerning trade policies and the international trading system.

SDG 12: Responsible Consumption and Production

- The article touches upon the need for resilient and efficient supply chains. It mentions “localized production,” “supply chain bottlenecks,” and investments in “agricultural infrastructure and storage.” These topics connect to the goal of ensuring sustainable production patterns and reducing food losses along the supply chain.

2. What specific targets under those SDGs can be identified based on the article’s content?

SDG 2: Zero Hunger

- Target 2.b: “Correct and prevent trade restrictions and distortions in world agricultural markets…” This target is directly addressed through the article’s focus on “retaliatory tariffs,” such as “China’s 50% duties on U.S. soybeans,” the “EU’s bans on hormone-treated beef,” and the potential reimposition of “reciprocal tariffs.” These are all examples of trade restrictions and distortions that the target aims to correct.

- Target 2.c: “Adopt measures to ensure the proper functioning of food commodity markets…in order to help limit extreme food price volatility.” The article highlights the failure to meet this target by describing significant “price swings” and “commodity volatility,” citing how “Cocoa prices surged over 100% in 2024” and the existence of “wheat volatility linked to Ukraine’s ongoing conflict.” It also mentions government measures like “China’s expanded stockpile budgets and India’s record rice reserves,” which are actions taken in response to market instability.

SDG 17: Partnerships for the Goals

- Target 17.10: “Promote a universal, rules-based, open, non-discriminatory and equitable multilateral trading system…” The article illustrates the challenges to this target by describing a landscape of “geopolitical tension,” “trade disputes,” and unilateral tariffs that undermine a rules-based system. The “surged” U.S. agricultural trade deficit is presented as a consequence of these disruptions.

- Target 17.11: “Significantly increase the exports of developing countries…” The article provides a direct example of this target being met as a consequence of trade shifts. It states that due to U.S.-China trade disputes, “Brazil and Argentina now supplying 60% of China’s soybean imports, up from 40% in 2022,” representing a significant increase in the exports of these developing/emerging economies.

SDG 12: Responsible Consumption and Production

- Target 12.3: “…reduce food losses along production and supply chains, including post-harvest losses.” This target is implied through the discussion of solutions to market disruptions. The article notes that “Governments worldwide are prioritizing food security, creating demand for agricultural infrastructure and storage,” which are essential investments for reducing post-harvest food losses. The mention of “supply chain bottlenecks” also points to inefficiencies where food loss can occur.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

Indicators for SDG 2 Targets

- Indicator for Target 2.b (Producer protection): The level of tariffs is a direct indicator. The article specifies “China’s 50% duties on U.S. soybeans” as a concrete measure of trade restriction.

- Indicator for Target 2.c (Food price volatility): The article provides a direct measure of price volatility with the statement that “Cocoa prices surged over 100% in 2024.” The level of national food reserves is another indicator, mentioned as “India’s record rice reserves.”

Indicators for SDG 17 Targets

- Indicator for Target 17.10 (Trade system health): The “U.S. agricultural trade deficit,” which reached an “estimated $49.5 billion in FY 2025,” serves as an indicator of market distortions and the breakdown of a balanced multilateral trading system.

- Indicator for Target 17.11 (Developing country exports): A specific metric is provided to measure the increase in exports from developing countries: the change in market share for soybean imports to China, where “Brazil and Argentina now supplying 60%… up from 40% in 2022.”

Indicators for SDG 12 Targets

- Indicator for Target 12.3 (Food loss reduction): While not providing a direct metric of food loss, the article implies an input indicator: investment in infrastructure. The “demand for agricultural infrastructure and storage” can be measured to track efforts towards reducing post-harvest losses.

4. Table of SDGs, Targets, and Indicators

| SDGs | Targets | Indicators Identified in the Article |

|---|---|---|

| SDG 2: Zero Hunger | 2.b: Correct and prevent trade restrictions and distortions in world agricultural markets. | The level of retaliatory tariffs (e.g., “China’s 50% duties on U.S. soybeans”). |

| 2.c: Adopt measures to ensure the proper functioning of food commodity markets… to help limit extreme food price volatility. | The percentage increase in commodity prices (e.g., “Cocoa prices surged over 100% in 2024”); Level of national food reserves (e.g., “India’s record rice reserves”). | |

| SDG 17: Partnerships for the Goals | 17.10: Promote a universal, rules-based, open, non-discriminatory and equitable multilateral trading system. | The size of the agricultural trade deficit (e.g., “surged to historic levels, reaching an estimated $49.5 billion”). |

| 17.11: Significantly increase the exports of developing countries. | Change in a country’s share of global commodity trade (e.g., “Brazil and Argentina now supplying 60% of China’s soybean imports, up from 40% in 2022”). | |

| SDG 12: Responsible Consumption and Production | 12.3: Reduce food losses along production and supply chains, including post-harvest losses. | Demand and investment in “agricultural infrastructure and storage” as a proxy for efforts to reduce post-harvest loss. |

Source: ainvest.com

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0

:quality(70):focal(289x270:299x280)/cloudfront-us-east-1.images.arcpublishing.com/shawmedia/H7NH74ZRH5CNJBTEBSN7OYFHL4.jpg?#)