The HELOC rate today, July 21 2025: Home equity line of credit rates continue to be stable – Yahoo Finance

Analysis of Home Equity Lines of Credit (HELOCs) and their Alignment with Sustainable Development Goals

Executive Summary: Current Market Conditions and Sustainable Potential

An examination of the current financial landscape reveals that Home Equity Line of Credit (HELOC) interest rates remain below 8.75%, with the Federal Reserve maintaining a cautious policy stance. Despite this, discussions regarding potential rate cuts persist. This environment, coupled with record levels of home equity exceeding $34 trillion, presents a unique opportunity for homeowners to leverage financial instruments like HELOCs. This report analyzes the mechanics of HELOCs and frames their utilization as a strategic tool for advancing several United Nations Sustainable Development Goals (SDGs), transforming personal financial decisions into actions that support global sustainability targets.

HELOCs as a Catalyst for Sustainable Development

By retaining low-interest primary mortgages, homeowners can access locked-in equity through HELOCs. This capital can be strategically deployed to foster economic resilience, promote environmental sustainability, and enhance social well-being, directly contributing to the SDG framework.

Fostering Economic Growth and Resilience (SDG 1, SDG 8)

Access to capital is fundamental to eradicating poverty (SDG 1) and promoting decent work and economic growth (SDG 8). A HELOC provides a flexible credit line that can empower homeowners to:

- Invest in education or vocational training to enhance skills and employability.

- Provide seed funding for small business ventures, creating jobs and fostering local economic activity.

- Establish a financial safety net to absorb economic shocks, preventing a slide into poverty.

This mechanism allows for wealth-building while maintaining the stability of a low-rate primary mortgage, reinforcing household financial security.

Promoting Sustainable Cities and Green Infrastructure (SDG 7, SDG 11, SDG 13)

A primary use for HELOC funds is home improvement. This presents a significant opportunity to advance goals for affordable and clean energy (SDG 7), sustainable cities and communities (SDG 11), and climate action (SDG 13). Homeowners can finance upgrades that include:

- Installation of solar panels and other renewable energy systems.

- Upgrades to energy-efficient appliances, windows, and insulation.

- Water conservation systems and retrofits.

- Climate-resilient modifications to improve housing durability.

By improving existing housing stock, this approach reduces the carbon footprint of communities and avoids the environmental impact of new construction.

Key Financial Considerations for Responsible Utilization

To effectively leverage a HELOC for sustainable purposes, borrowers must navigate the market responsibly. This involves careful consideration of rates, terms, and lenders, ensuring financial decisions are both prudent and impactful.

Current Market Rates and Lender Comparison

Rates are highly variable and depend on creditworthiness, debt levels, and the loan-to-value ratio. Diligent comparison is essential.

- National Average (Example): Bank of America, a major lender, reports an average variable APR of 8.72% following a 6.49% six-month introductory period.

- Promotional Offer (Example): FourLeaf Credit Union offers an introductory rate of 6.49% for 12 months on lines up to $500,000.

- Rate Spectrum: Borrowers may encounter rates ranging from approximately 7% to as high as 18%.

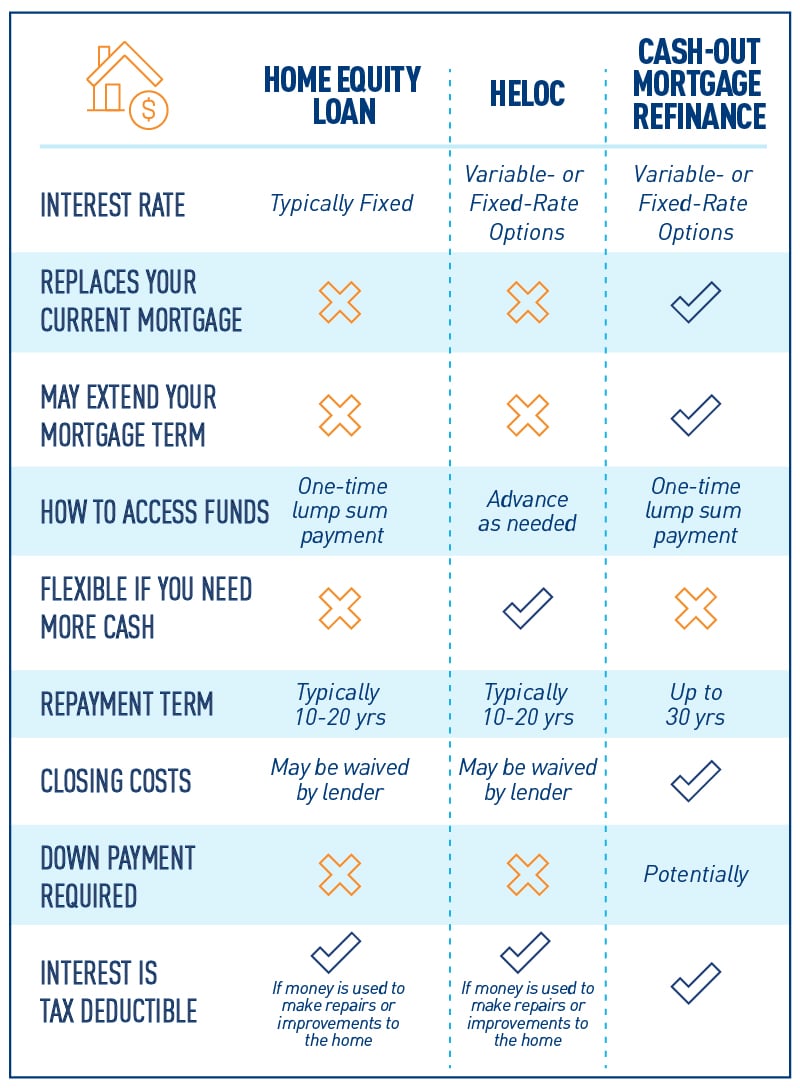

Understanding HELOC Structure and Terms

Responsible borrowing, in line with SDG 12 (Responsible Consumption and Production), requires a full understanding of the product.

- Index and Margin: HELOC rates are typically based on an index (e.g., the prime rate, currently 7.50%) plus a lender’s margin.

- Introductory vs. Variable Rates: Be aware of the limited duration of low introductory rates and the subsequent transition to a higher, adjustable rate.

- Draw and Repayment Periods: A typical structure involves a 10-year draw period, where funds can be accessed as needed, followed by a 20-year repayment period.

- Disciplined Repayment: To avoid long-term debt for short-term benefits, it is advisable to borrow only what is necessary and create a plan to repay the balance swiftly, particularly for non-asset-building expenditures.

Analysis of Sustainable Development Goals (SDGs) in the Article

1. Which SDGs are addressed or connected to the issues highlighted in the article?

-

SDG 8: Decent Work and Economic Growth

- The article focuses on financial products like Home Equity Lines of Credit (HELOCs) offered by domestic financial institutions such as Bank of America and FourLeaf Credit Union. It discusses interest rates, the role of the Federal Reserve, and the mechanics of accessing credit. This relates to the broader economic framework and the role of financial services in the economy.

-

SDG 11: Sustainable Cities and Communities

- The article explicitly mentions that a HELOC can be used for “home improvements, repairs, and upgrades.” This directly connects to the goal of ensuring adequate and safe housing by providing a financial mechanism for homeowners to maintain and improve their properties.

2. What specific targets under those SDGs can be identified based on the article’s content?

-

Target 8.10: Strengthen the capacity of domestic financial institutions to encourage and expand access to banking, insurance and financial services for all.

- The entire article serves as an example of this target in action. It details how financial institutions are providing a specific service (HELOCs) to homeowners, thereby expanding access to credit. The mention of different lenders (“Bank of America, the largest HELOC lender,” “FourLeaf Credit Union”) and the advice to “shop around” highlights the existence of a competitive market for these financial services.

-

Target 11.1: By 2030, ensure access for all to adequate, safe and affordable housing and basic services and upgrade slums.

- The article supports the “adequate” and “safe” housing aspect of this target. It states, “…you can use the cash drawn from your equity for things like home improvements, repairs, and upgrades.” By providing homeowners with a financial tool to fund these activities, HELOCs contribute to the upkeep and improvement of the existing housing stock, preventing deterioration and enhancing living conditions.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

-

Indicators for Target 8.10

- Value of Home Equity: The article states that homeowners have “more than $34 trillion at the end of 2024” in home equity. This figure serves as a proxy indicator for the total volume of personal assets that could potentially be leveraged through financial services like HELOCs.

- Interest Rates and Product Availability: The article provides specific data points on the cost of credit, such as “today’s average APR on a 10-year draw HELOC is 8.72%” from Bank of America and an introductory rate of “6.49% for 12 months” from FourLeaf Credit Union. The range of rates (“from nearly 7% to as much as 18%”) indicates the functioning and accessibility of the credit market for different consumers.

-

Indicators for Target 11.1

- Financial Allocation for Housing Upgrades: The article provides a specific example of a homeowner taking out a “$50,000” line of credit. While not a national statistic, this figure serves as an indicator of the potential scale of financial investment an individual household can make towards home improvements and repairs, which is a primary use case for HELOCs mentioned in the text.

4. Create a table with three columns titled ‘SDGs, Targets and Indicators” to present the findings from analyzing the article.

| SDGs | Targets | Indicators |

|---|---|---|

| SDG 8: Decent Work and Economic Growth | 8.10: Strengthen the capacity of domestic financial institutions to encourage and expand access to banking, insurance and financial services for all. |

|

| SDG 11: Sustainable Cities and Communities | 11.1: Ensure access for all to adequate, safe and affordable housing and basic services and upgrade slums. |

|

Source: finance.yahoo.com

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0