Economic Developments – October 2024

Growth Outlook Upgraded on Revisions to Income Data

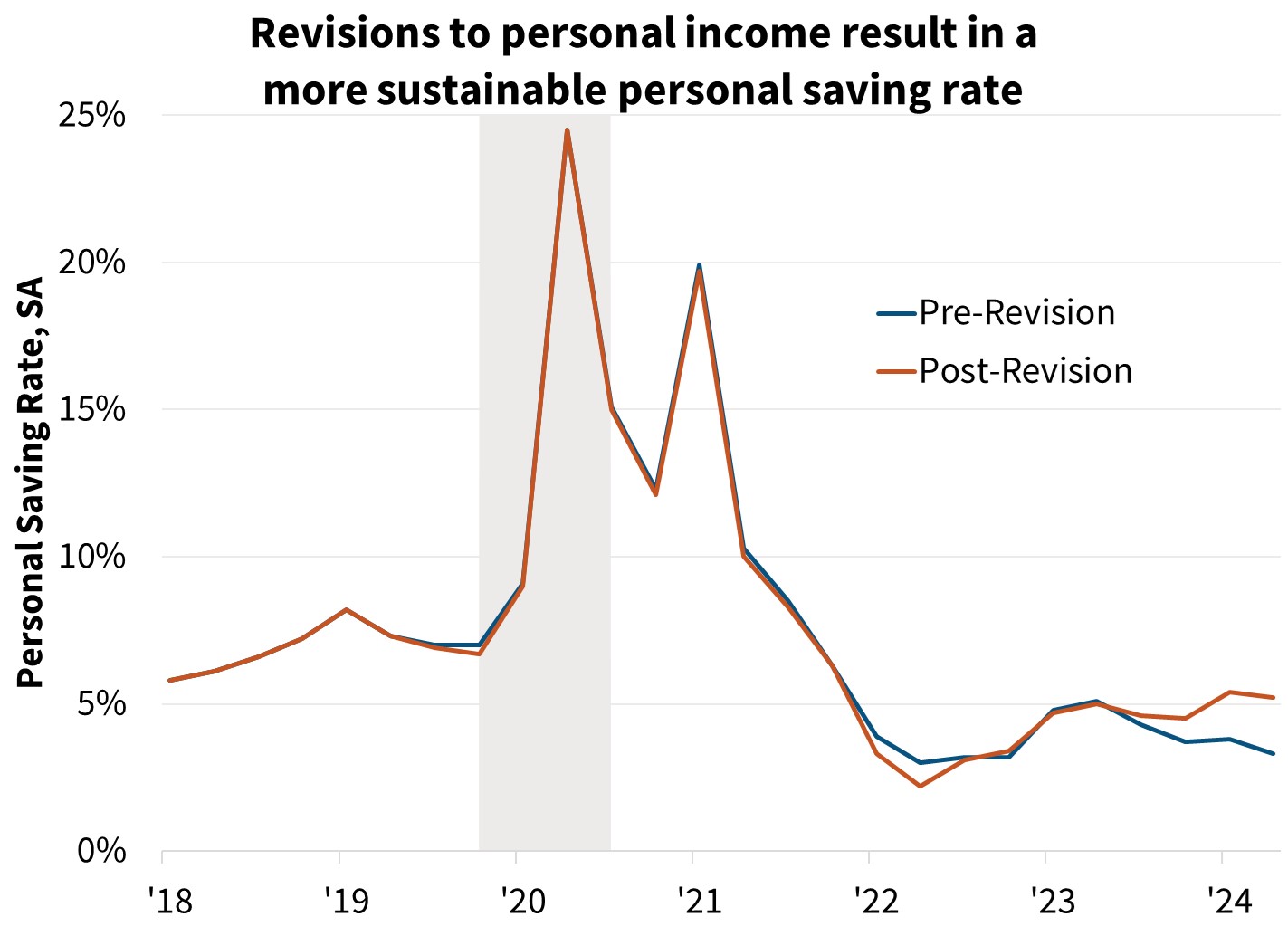

We have upgraded our economic growth outlook for 2024 and 2025 in large part due to significant revisions to recent personal income data as part of the Bureau of Economic Analysis’s (BEA) annual revision to the national accounts. Pre-revision data had shown that, while personal consumption expenditures continued to grow at a robust pace over the past year, disposable personal income growth lagged meaningfully behind. This had pushed the reported personal saving rate down to 3.3 percent in the second quarter, nearly four percentage points below its 2019 level. We viewed this relationship as unsustainable and previously called for a retrenchment in consumption to a pace below the trend growth rate over the course of several quarters. However, post-revision data now show the saving rate at 5.2 percent in Q2. While still somewhat below the pre-pandemic level, this higher saving rate points to far less of a disconnect between consumers’ income and spending trends. As such, we no longer believe that consumption growth will need to slow as much to bring this relationship into balance.

Impact on Sustainable Development Goals (SDGs)

- SDG 8: Decent Work and Economic Growth – The upgraded growth outlook indicates positive progress towards achieving this goal.

- SDG 10: Reduced Inequalities – The revisions to income data suggest a reduction in income inequality, contributing to this goal.

- SDG 12: Responsible Consumption and Production – The higher saving rate indicates a more sustainable consumption pattern, aligning with this goal.

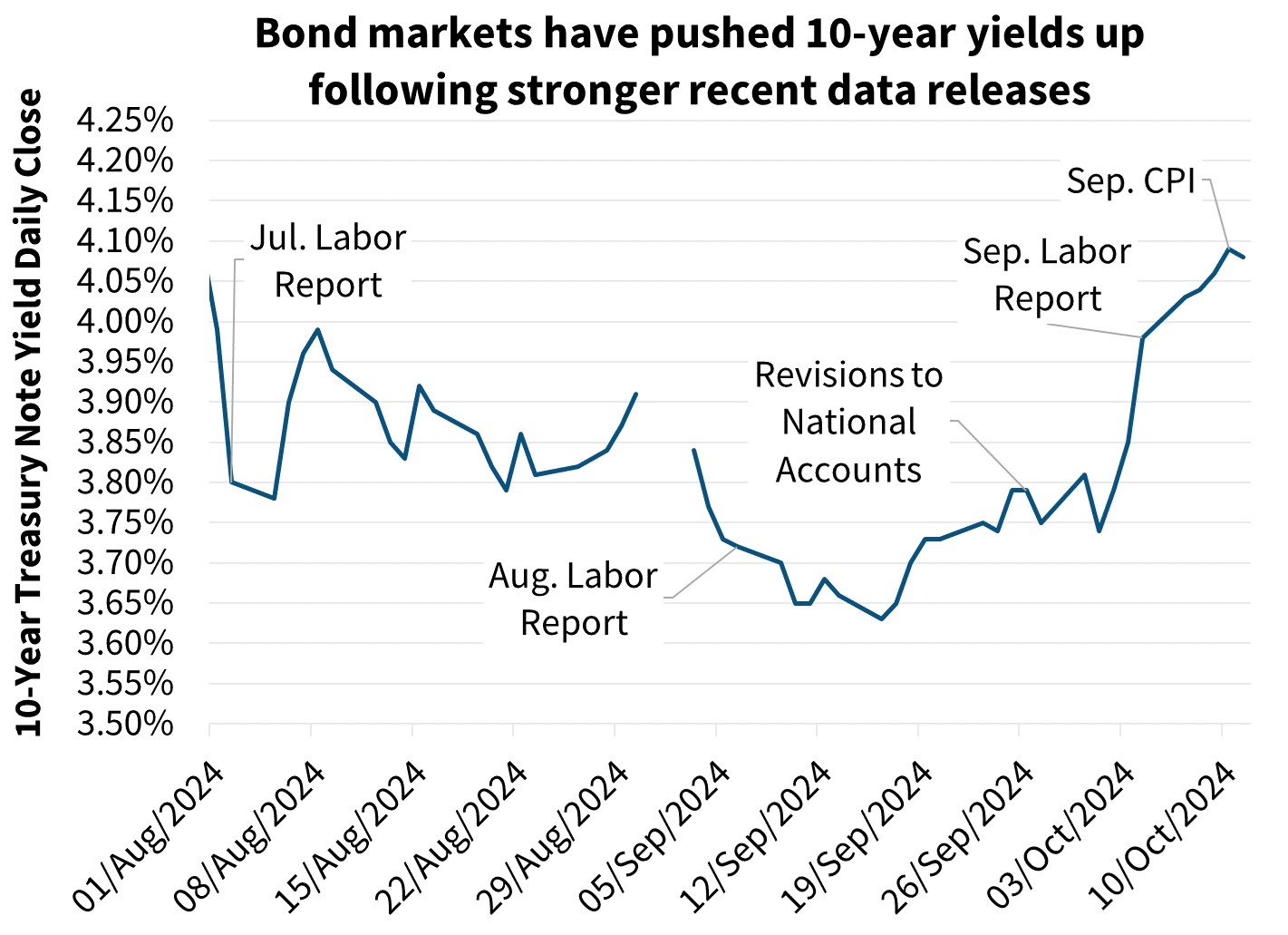

Economic and Labor Market Data Push Rates Higher after Brief Reprieve

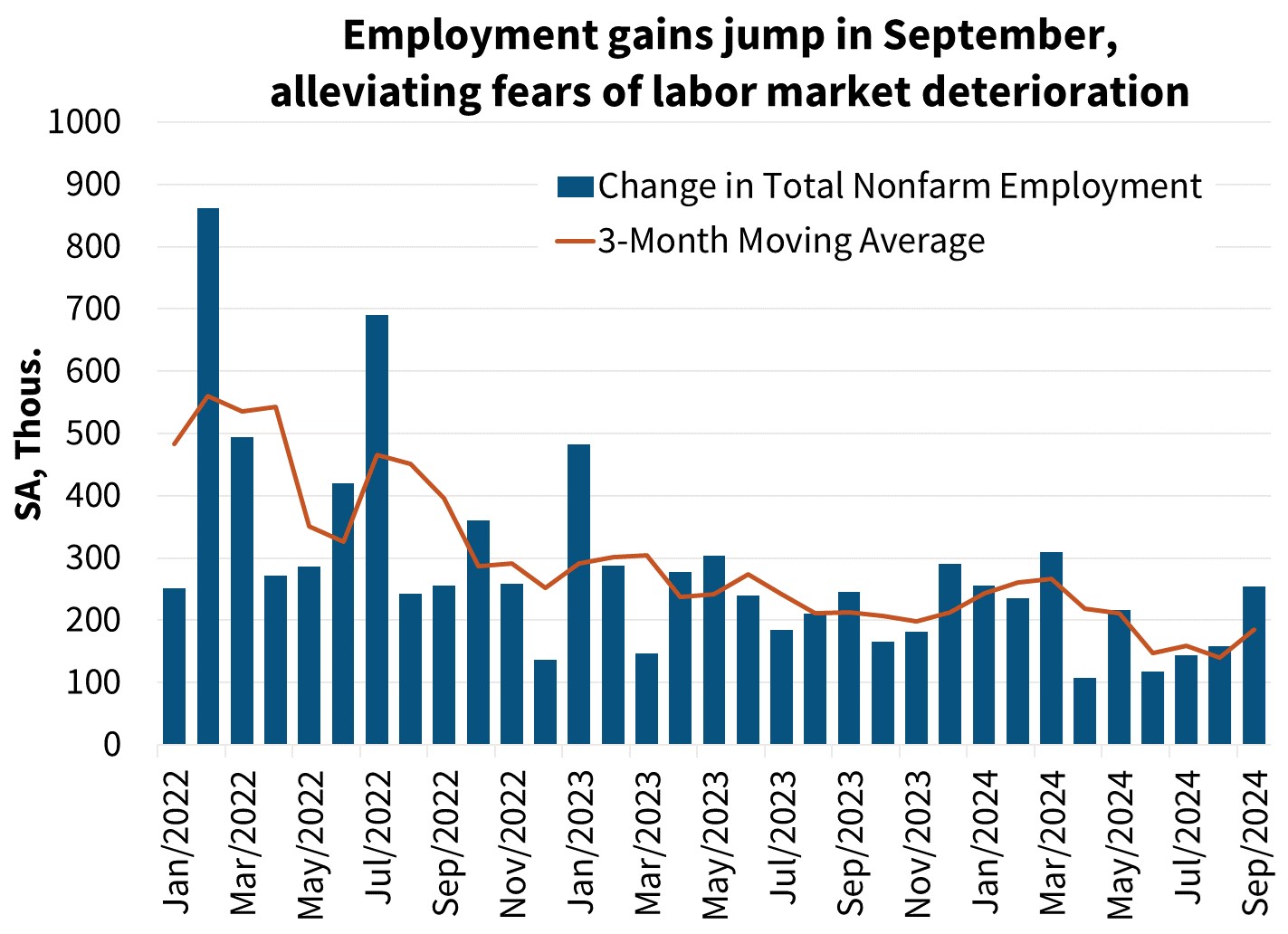

Nonfarm payroll employment rose by 254,000 in September, well above market expectations. Additionally, the prior two months of data were revised upward by a combined 72,000 jobs, and the unemployment rate declined one-tenth to 4.2 percent. Following fears that the labor market was slowing too quickly when unemployment hit 4.4 percent in July, the August and September labor reports have largely assuaged those concerns. Still, a broad range of labor market indicators continue to suggest that conditions are meaningfully looser now than in 2023. The quits rate, a useful indicator for both future wage growth and confidence in the labor market, declined to 1.9 percent in August, four-tenths below its pre-pandemic level, and the lowest since July 2015 (excluding the pandemic period). The Kansas City Fed Labor Market Conditions Index, an aggregate of 24 monthly measures of labor market conditions, remains in positive territory (signaling better than long-run average conditions) but is nearly 50 percent lower than it was a year ago in September 2023. On balance, we continue to expect a gradual slowing in employment growth. Similar to our expectation that the economy will return to roughly its long-run growth rate, we believe the unemployment rate will rise modestly to 4.4 percent, roughly our current estimate of the natural rate of unemployment.

Impact on Sustainable Development Goals (SDGs)

- SDG 1: No Poverty – The employment gains and declining unemployment rate contribute to reducing poverty.

- SDG 8: Decent Work and Economic Growth – The positive labor market data aligns with this goal.

Home Price Outlook Upgraded as Sales Expected to Remain Subdued

As measured by the Fannie Mae Home Price Index (FNM-HPI), home prices increased 5.9 percent year over year in Q3 2024, a deceleration compared to the previous quarter’s downwardly revised year-over-year growth rate of 6.3 percent. We have updated our quarterly home price outlook and now expect modestly strong home price appreciation through 2025. However, revisions to historical data on balance were to the downside, leading to a modest downward revision to our 2024 expectation for year-total home price growth, but an upward revision to our 2025 outlook. We are expecting deceleration of home price growth as affordability continues to be stretched and inventories of homes available for sale are rising in some regions. However, the overall low level of available homes for sale is still bolstering home price appreciation, especially as income growth and employment remain strong.

Impact on Sustainable Development Goals (SDGs)

- SDG 11: Sustainable Cities and Communities – The home price outlook and availability of affordable housing are relevant to this goal.

- SDG 12: Responsible Consumption and Production – The consideration of affordability and inventories aligns with this goal.

Annual Benchmarking Update to Mortgage Originations Estimate

We have updated our estimate of 2023 mortgage origination volumes as part of our annual benchmarking exercise to incorporate the latest Home Mortgage Disclosure Act (HMDA) data. Specifically, we have revised upward total mortgage volumes by $33 billion to $1.5 trillion in 2023, with the purchase market being revised upward by $60 billion to $1.28 trillion and the refinance market being revised downward by $27 billion to $221 billion. As part of this benchmarking work, our estimate of the share of homes purchased with cash instead of a mortgage was revised downward somewhat relative to last month’s forecast.

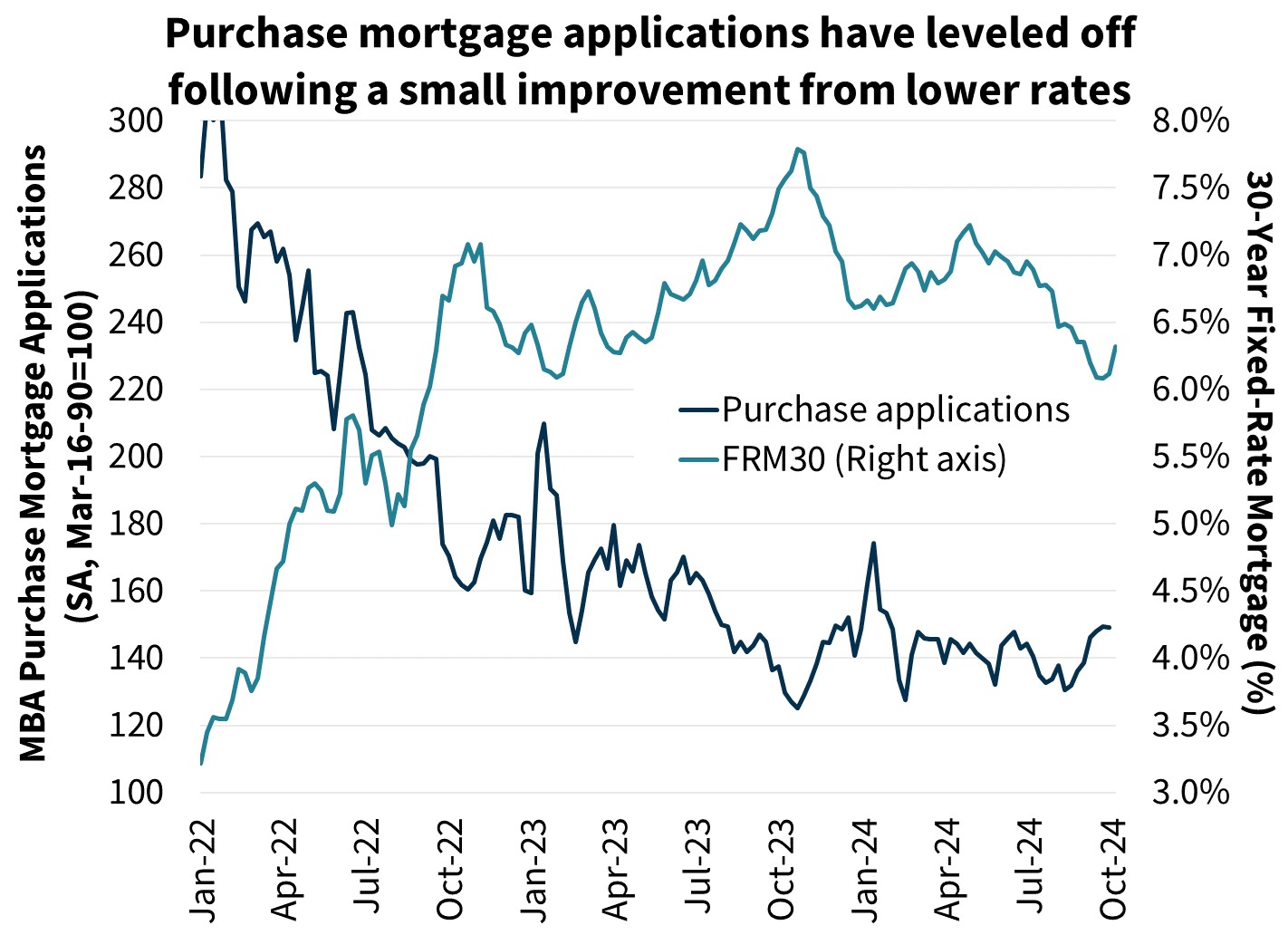

In 2025, we expect purchase volumes to grow to $1.5 trillion, as home sales rebound somewhat from recent lows and solid home price appreciation continues. Refinance volumes are expected to grow to $625 billion in 2025, as a gradually declining mortgage rate path continues to be supportive of refinance activity. While refinance application activity has dipped as of late, as seen in the Refinance Application-Level Index (or RALI), application activity is still well above levels seen earlier in 2024.

Impact on Sustainable Development Goals (SDGs)

- SDG 1: No Poverty – The mortgage origination volumes and home sales rebound contribute to reducing poverty.

- SDG 8: Decent Work and Economic Growth – The mortgage market activity and home sales support this goal.

SDGs, Targets, and Indicators

SDGs Addressed:

- SDG 8: Decent Work and Economic Growth

- SDG 10: Reduced Inequalities

- SDG 11: Sustainable Cities and Communities

- SDG 12: Responsible Consumption and Production

Targets Identified:

- SDG 8.1: Sustain per capita economic growth in accordance with national circumstances and, in particular, at least 7 percent gross domestic product growth per annum in the least developed countries

- SDG 10.1: By 2030, progressively achieve and sustain income growth of the bottom 40 percent of the population at a rate higher than the national average

- SDG 11.1: By 2030, ensure access for all to adequate, safe and affordable housing and basic services and upgrade slums

- SDG 12.2: By 2030, achieve the sustainable management and efficient use of natural resources

Indicators:

- GDP growth rate

- Personal income growth rate

- Personal saving rate

- Unemployment rate

- Quits rate

- 10-year Treasury yield

- Mortgage rates

- Home price appreciation

- Purchase mortgage volumes

- Refinance volumes

Analysis

1. Which SDGs are addressed or connected to the issues highlighted in the article?

The issues highlighted in the article are connected to SDG 8 (Decent Work and Economic Growth), SDG 10 (Reduced Inequalities), SDG 11 (Sustainable Cities and Communities), and SDG 12 (Responsible Consumption and Production).

2. What specific targets under those SDGs can be identified based on the article’s content?

Based on the article’s content, the specific targets that can be identified are:

- SDG 8.1: Sustain per capita economic growth

- SDG 10.1: Achieve income growth for the bottom 40 percent of the population

- SDG 11.1: Ensure access to adequate housing and basic services

- SDG 12.2: Achieve sustainable management and efficient use of natural resources

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

Yes, there are several indicators mentioned or implied in the article that can be used to measure progress towards the identified targets. These indicators include GDP growth rate, personal income growth rate, personal saving rate, unemployment rate, quits rate, 10-year Treasury yield, mortgage rates, home price appreciation, purchase mortgage volumes, and refinance volumes.

Table: SDGs, Targets, and Indicators

| SDGs | Targets | Indicators |

|---|---|---|

| SDG 8: Decent Work and Economic Growth | SDG 8.1: Sustain per capita economic growth in accordance with national circumstances and, in particular, at least 7 percent gross domestic product growth per annum in the least developed countries | GDP growth rate |

| SDG 10: Reduced Inequalities | SDG 10.1: By 2030, progressively achieve and sustain income growth of the bottom 40 percent of the population at a rate higher than the national average | Personal income growth rate |

| SDG 11: Sustainable Cities and Communities | SDG 11.1: By 2030, ensure access for all to adequate, safe and affordable housing and basic services and upgrade slums | Home price appreciation |

| SDG 12: Responsible Consumption and Production | SDG 12.2: By 2030, achieve the sustainable management and efficient use of natural resources | Purchase mortgage volumes, refinance volumes |

Source: fanniemae.com

![]()