Holiday week brings little change to home equity rates – Yahoo Finance

Report on Home Equity Market Stability and its Alignment with Sustainable Development Goals

1.0 Executive Summary

This report analyzes recent trends in the home equity market, noting a period of significant rate stability. This stability has profound implications for achieving several United Nations Sustainable Development Goals (SDGs), particularly those related to economic well-being, inequality, and sustainable communities. The analysis indicates that predictable and accessible home equity financing can serve as a crucial tool for empowering individuals and fostering inclusive economic growth, thereby contributing to SDG 1 (No Poverty), SDG 8 (Decent Work and Economic Growth), SDG 10 (Reduced Inequalities), and SDG 11 (Sustainable Cities and Communities).

2.0 Market Conditions and Rate Analysis

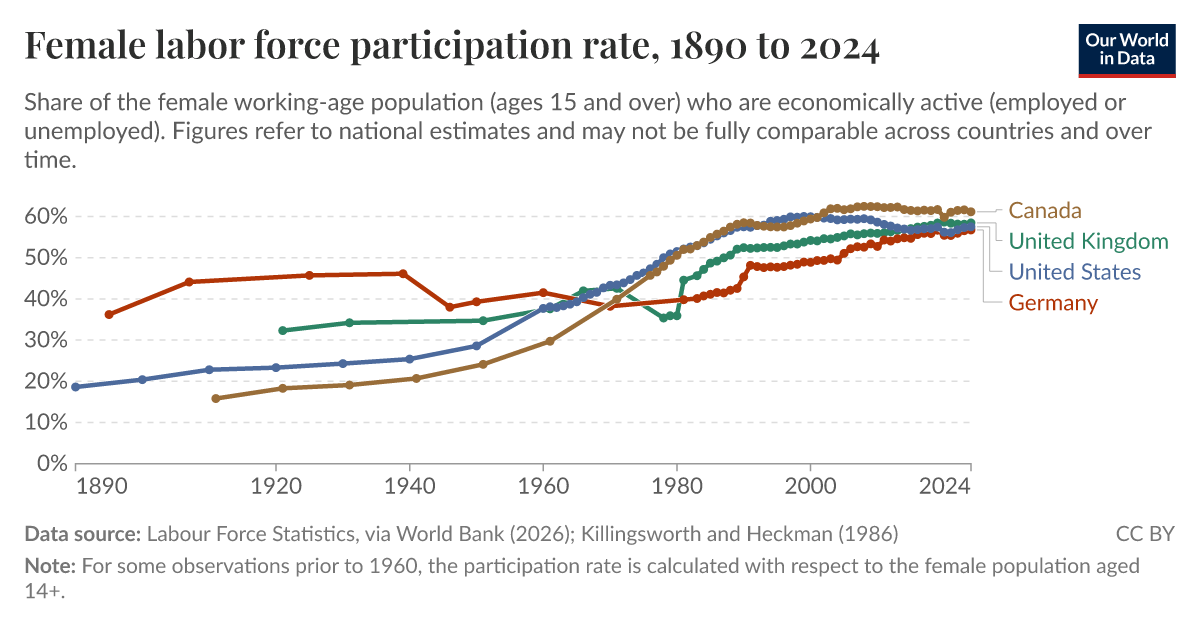

During the reporting period, the home equity market demonstrated minimal rate fluctuations. This stability provides a predictable environment for homeowners considering leveraging their property assets for financial needs. Such predictability is essential for long-term financial planning, a cornerstone of economic stability for households and communities.

2.1 Current Interest Rates

The national survey of lenders for a $30,000 loan amount reveals the following key rates:

- Home Equity Line of Credit (HELOC): Unchanged at 7.81%, marking its 52-week low.

- 5-Year Home Equity Loan: Marginally increased to 8.01%, remaining near a two-year low.

- 10-Year Home Equity Loan: Currently at 8.19%.

- 15-Year Home Equity Loan: Positioned at 8.14%.

2.2 Factors Influencing Market Stability

Several macroeconomic and market-specific factors contribute to the current rate environment:

- Monetary Policy: Actions by the Federal Reserve are a primary driver, particularly for variable-rate products like HELOCs. Recent rate cuts have contributed to the decline from 2024 highs.

- Lender Competition: Competitive pressures, promotional offers, and evolving underwriting standards among financial institutions also impact the rates available to consumers.

- Economic Indicators: The release of delayed economic data following the government shutdown may introduce new variables that could influence future policy decisions and market expectations.

3.0 Contribution to Sustainable Development Goals (SDGs)

The stability and accessibility of home equity financing are directly linked to the advancement of key SDGs. By providing a cost-effective alternative to unsecured debt, these financial products empower homeowners to improve their economic and social standing.

- SDG 1 (No Poverty) & SDG 10 (Reduced Inequalities): Access to affordable credit secured by a home is a vital mechanism for financial inclusion. It allows households to manage economic shocks, invest in education, or consolidate higher-interest debts, thereby preventing descents into poverty and reducing the wealth gap by enabling asset utilization.

- SDG 8 (Decent Work and Economic Growth): Home equity can serve as seed capital for entrepreneurship and small business development. A stable rate environment encourages such investment, fostering job creation and contributing to sustained, inclusive, and sustainable economic growth at the local level.

- SDG 11 (Sustainable Cities and Communities): Funds from home equity loans are often used for home improvements. This not only improves housing quality and safety but can also be directed towards energy-efficient upgrades, contributing to more sustainable housing stock and resilient communities.

4.0 Conclusion and Recommendations

The current stability in the home equity market presents a significant opportunity to advance sustainable development objectives. Financial experts advise that the decision to utilize home equity should be based on a legitimate need and a holistic assessment of one’s financial situation. This aligns with the principles of responsible financial management. To maximize the positive impact on the SDGs, it is recommended that borrowers and lenders alike consider how these funds can be used for long-term value creation, such as improving household resilience, fostering economic opportunity, and enhancing the sustainability of communities.

Analysis of Sustainable Development Goals in the Article

1. Which SDGs are addressed or connected to the issues highlighted in the article?

The article on home equity rates connects to the following Sustainable Development Goals (SDGs):

- SDG 8: Decent Work and Economic Growth: The article discusses access to credit through home equity loans and lines of credit (HELOCs). Access to affordable financial services is a crucial component of economic growth, as it allows individuals to invest, manage their finances, and potentially start or support small businesses. The article’s focus on interest rates, lender competition, and the role of the Federal Reserve relates directly to the health and accessibility of financial systems that underpin economic activity.

- SDG 11: Sustainable Cities and Communities: The financial products discussed are directly tied to housing, a central element of this goal. Home equity loans are often used for home improvements, repairs, or renovations. By providing a “cost-effective borrowing option,” these financial tools can help homeowners maintain and improve their properties, contributing to the overall quality, safety, and adequacy of the housing stock within a community.

2. What specific targets under those SDGs can be identified based on the article’s content?

Based on the article’s focus, the following specific SDG targets can be identified:

- Target 8.10: Strengthen the capacity of domestic financial institutions to encourage and expand access to banking, insurance and financial services for all.

- The article directly addresses this target by discussing the products (HELOCs, home equity loans) offered by domestic financial institutions like banks. It highlights factors that influence the accessibility and cost of these services, such as “the Federal Reserve’s actions,” “lender competition, promotional offers and underwriting standards.” The advice to “shop around and comparing multiple offers” further emphasizes the role of a competitive financial sector in providing services to consumers.

- Target 11.1: By 2030, ensure access for all to adequate, safe and affordable housing and basic services and upgrade slums.

- While the article does not discuss slums, it is fundamentally about the affordability of housing finance. It states that HELOCs and home equity loans “tend to be much less expensive” than other forms of credit and represent the “most cost-effective borrowing option” for homeowners needing credit. This affordability is key to enabling homeowners to invest in their properties, ensuring they remain adequate and safe, which is a core component of this target.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

Yes, the article provides several specific quantitative indicators that can be used to measure the cost and accessibility of financial products related to the identified targets.

- Interest Rates for Financial Products: The primary indicators mentioned are the interest rates for various home equity products. These rates are a direct measure of the cost of credit, which is a key component of access to financial services (Target 8.10) and housing affordability (Target 11.1). The article explicitly provides:

- The current rate for a $30,000 HELOC: 7.81%

- The current rate for a five-year $30,000 home equity loan: 8.01%

- Rates for 10-year (8.19%) and 15-year (8.14%) home equity loans.

- Trends and Benchmarks in Interest Rates: The article also provides historical and comparative data that serve as indicators of market stability and trends over time. These include:

- Rates from four weeks ago (e.g., 7.90% for a HELOC).

- Rates from one year ago (e.g., 8.56% for a HELOC).

- The 52-week average and 52-week low for each product.

These trend indicators help measure the volatility and direction of borrowing costs, which reflects the overall health and stability of the financial system discussed in Target 8.10.

4. Summary Table of SDGs, Targets, and Indicators

| SDGs | Targets | Indicators |

|---|---|---|

| SDG 8: Decent Work and Economic Growth | Target 8.10: Strengthen the capacity of domestic financial institutions to encourage and expand access to banking, insurance and financial services for all. |

|

| SDG 11: Sustainable Cities and Communities | Target 11.1: By 2030, ensure access for all to adequate, safe and affordable housing and basic services and upgrade slums. |

|

Source: finance.yahoo.com

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0