Money Supply Growth: A Thesis With A Fatal Flaw – Real Investment Advice

Analysis of Modern Monetary Policy and Asset Allocation in the Context of Sustainable Development Goals

A recent financial market narrative suggests that rising government deficits and money supply growth necessitate a shift to hard assets like gold, silver, and bitcoin. This report examines the underlying economic principles of this thesis, evaluating its validity through the lens of the United Nations Sustainable Development Goals (SDGs). The analysis indicates that the popular narrative is based on a simplified view of modern economics and that current fiscal and monetary frameworks, when properly understood, are aligned with achieving long-term sustainable growth.

Monetary Policy and its Alignment with Sustainable Economic Growth (SDG 8)

The argument that an expanding money supply inherently debases a currency overlooks the mechanics of money creation in modern economies. This misunderstanding has significant implications for policies aimed at achieving SDG 8 (Decent Work and Economic Growth).

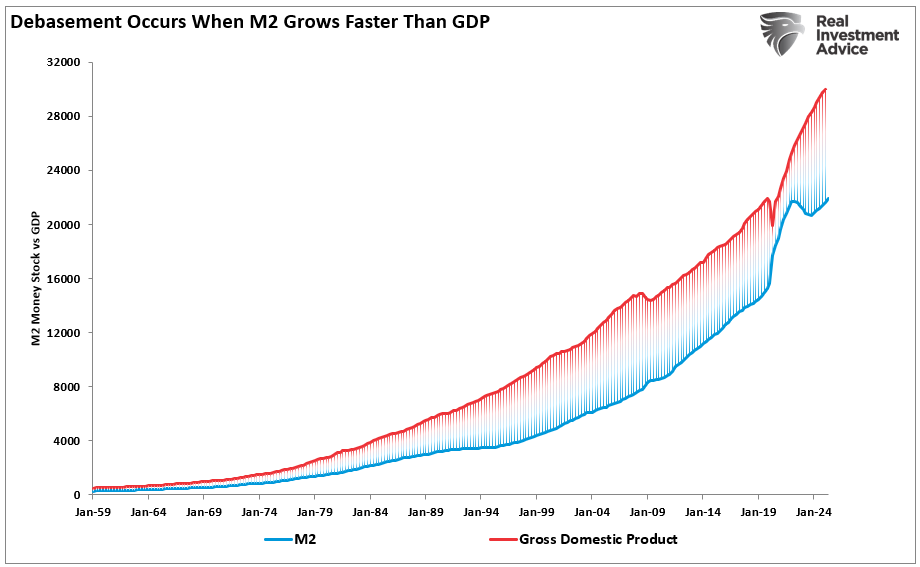

- Endogenous Money Creation: Money is not centrally “printed” but is created by commercial banks through lending in response to economic demand. This process, known as endogenous money creation, means that money supply growth is primarily an indicator of, rather than a cause of, economic activity.

- Supporting Economic Growth: A healthy, growing economy requires an expanding money supply to facilitate transactions, investment, and innovation. Aligning money supply with Gross Domestic Product (GDP) growth is essential for preventing deflation and supporting the creation of decent work, a core target of SDG 8. Historical data shows a strong correlation between the growth of the M2 money supply and U.S. economic growth.

- Global Financial Stability: The U.S. dollar’s role as the world’s primary reserve currency is a stabilizing force. It is used in the vast majority of global trade and foreign exchange transactions. This stability underpins the global financial system, which is critical for financing sustainable development initiatives worldwide.

The Role of Fiscal Deficits in Promoting Economic Stability and Reducing Inequality (SDG 9 & SDG 10)

Concerns over “out of control” government deficits often fail to recognize the accounting identity that a government deficit corresponds to a private-sector surplus. This dynamic is crucial for achieving SDG 10 (Reduced Inequalities) and SDG 9 (Industry, Innovation, and Infrastructure).

- Private Sector Surpluses: Government deficit spending transfers net financial assets to households and businesses. During economic downturns, this mechanism acts as a powerful stabilizer, supporting household balance sheets and preventing a deeper recession, thereby mitigating the impact on the most vulnerable populations and contributing to the goals of SDG 10.

- Financing Sustainable Development: The issuance of government securities (Treasuries) to fund deficits provides the global financial system with a highly demanded, safe asset. This deep and liquid market is the bedrock of global finance. Furthermore, deficits can be strategically deployed to fund long-term investments in renewable energy, resilient infrastructure, and technological innovation, directly advancing the objectives of SDG 9.

- Demand for U.S. Treasuries: Contrary to narratives of a sell-off, international demand for U.S. Treasuries remains robust. Foreign entities hold these assets as essential reserves for conducting international trade, which is predominantly settled in dollars. This persistent demand supports a stable financing environment for public investment.

Investment Risks and Global Financial Architecture (SDG 17)

The recommendation to abandon fiat currencies for hard assets like gold is predicated on a potential collapse of the current system. However, the price of these assets is intrinsically linked to the very system they are meant to replace, posing risks to investors and distracting from the global cooperation needed for SDG 17 (Partnerships for the Goals).

- Gold’s Dependency on the Dollar: Gold is priced in U.S. dollars, and its value has a historically inverse correlation with the dollar’s strength and real interest rates. A stronger dollar or higher real rates increase the opportunity cost of holding a non-yielding asset like gold, which can lead to price declines.

- Threat of Dollar Strength: A potential rally in the U.S. dollar, driven by stronger relative economic growth or interest rate differentials, could significantly undermine the investment case for gold and other hard assets. This dynamic highlights the continued centrality of the dollar in the global financial system.

- Distraction from Productive Investment: A fear-driven flight to non-productive assets like gold can divert capital away from investments in businesses, technologies, and infrastructure that generate sustainable growth and contribute to achieving the SDGs. A stable and predictable global financial system, as envisioned in SDG 17, relies on capital flowing toward productive uses.

Conclusion: A Framework for Sustainable Investment

The narrative promoting a flight to hard assets is based on a misinterpretation of the functions of money supply and government deficits in a modern economy. A more nuanced analysis reveals that these economic levers are integral to fostering the stable and inclusive growth required to meet the Sustainable Development Goals. For investors, focusing on economic fundamentals rather than fear-driven narratives is paramount for both wealth preservation and contributing to a sustainable future.

- Assess Economic Fundamentals: Investment decisions should be based on the alignment of money supply with economic growth, not on the absolute level of money supply in isolation. This approach supports policies geared towards SDG 8.

- Monitor Real Interest Rates and Currency Cycles: The performance of assets like gold is heavily influenced by real interest rates and the U.S. dollar’s cycle. Understanding these macroeconomic drivers is critical.

- Evaluate Fiscal Policy’s Impact: Analyze government debt in the context of its contribution to long-term economic capacity and social well-being, key components of SDGs 9 and 10.

- Prioritize Productive Assets: Maintain a diversified portfolio where hard assets serve as a hedge rather than a core holding, ensuring that capital remains allocated to productive enterprises that drive sustainable development.

- Support Global Financial Stability: Recognize the role of the U.S. dollar and Treasury market in providing global financial stability, a necessary precondition for the international cooperation required by SDG 17.

SDGs Addressed in the Article

- SDG 8: Decent Work and Economic Growth: The article’s central theme is the relationship between monetary policy, government deficits, and sustained economic growth (measured by GDP). It analyzes how money supply reflects economic expansion and how fiscal policy can support economic activity.

- SDG 17: Partnerships for the Goals: The article discusses the global financial system, focusing on the role of the U.S. dollar, international trade, foreign exchange reserves, and the global demand for U.S. Treasuries. It also directly addresses the importance of long-term debt sustainability.

- SDG 10: Reduced Inequalities: The article touches upon fiscal policies that can impact household wealth. It explains how government deficit spending, through transfer payments, can directly increase private-sector savings and support household financial stability.

Specific SDG Targets Identified

SDG 8: Decent Work and Economic Growth

- Target 8.1: Sustain per capita economic growth. The entire article is framed around understanding the drivers of economic prosperity and growth. It argues that “money supply growth is primarily a reflection of economic growth” and advises investors to “Track economic growth and money supply together.” The analysis consistently uses GDP as the primary measure of economic health.

- Target 8.10: Strengthen the capacity of domestic financial institutions. The article explains the mechanics of the modern financial system, noting that “commercial banks extending credit when they see viable opportunities” is the primary driver of money creation. This highlights the central role of financial institutions in facilitating the economic activity necessary for growth.

SDG 17: Partnerships for the Goals

- Target 17.4: Assist developing countries in attaining long-term debt sustainability. The article directly addresses this concept in a developed country context, which is a principle of global financial stability. It advises investors to “Assess debt sustainability” and clarifies that “The real risk is debt growing faster than the economy.” This focus on sustainable fiscal policy is central to the target.

- Target 17.13: Enhance global macroeconomic stability. The article analyzes the stability of the global financial system, which is anchored by the U.S. dollar. It provides evidence of this stability by stating the dollar is used in “88% of global foreign exchange transactions, 58% of international exchange reserves, and 54% of global trade,” and that demand for U.S. Treasuries remains robust globally.

SDG 10: Reduced Inequalities

- Target 10.4: Adopt policies, especially fiscal, wage and social protection policies, and progressively achieve greater equality. The article provides a direct example of this target in action. It explains how fiscal policy in the form of “Record government spending and transfer payments” during 2020-2021, including “stimulus checks and unemployment benefits,” directly led to households accumulating “trillions in excess savings,” thereby supporting the financial well-being of the private sector.

Indicators for Measuring Progress

Indicators for SDG 8

- Annual growth rate of GDP: This is the most prominent indicator used throughout the article. The text repeatedly compares money supply (M2) to GDP, stating, “Since 1959, the money supply has grown in alignment with economic growth.” The provided charts explicitly track GDP growth.

- Money Supply (M2): The article uses M2 as a key indicator of economic activity. It presents data on “M2 as a percentage of GDP” and the correlation between M2 and GDP growth rates to argue that money supply is a sign of economic vitality, not debasement.

Indicators for SDG 17

- Debt-to-GDP Ratio (Implied): While not named explicitly, the indicator is strongly implied in the advice to “track whether fiscal policy supports long-term growth” and the warning that “The real risk is debt growing faster than the economy.” This comparison is the essence of the debt-to-GDP ratio.

- Share of U.S. Dollar in International Reserves: The article explicitly cites the dollar’s share of global finance as an indicator of macroeconomic stability. It states that the dollar accounts for “58% of international exchange reserves,” demonstrating its central role in the global financial system.

Indicators for SDG 10

- Household Saving Rate: The article uses this as a direct indicator of the impact of fiscal and social protection policies. It notes that government transfer payments “pushed the household saving rate to an all-time high of 33%,” demonstrating how deficit spending became private wealth.

Summary Table of SDGs, Targets, and Indicators

| SDGs | Targets | Indicators |

|---|---|---|

| SDG 8: Decent Work and Economic Growth | 8.1: Sustain per capita economic growth. | Annual growth rate of GDP; Money Supply (M2) growth relative to GDP. |

| SDG 17: Partnerships for the Goals | 17.4: Attain long-term debt sustainability. 17.13: Enhance global macroeconomic stability. |

Debt-to-GDP ratio (implied by “debt growing faster than the economy”); Share of U.S. Dollar in international reserves (cited as 58%). |

| SDG 10: Reduced Inequalities | 10.4: Adopt policies, especially fiscal and social protection policies. | Household saving rate (cited as reaching 33% due to government transfer payments). |

Source: realinvestmentadvice.com

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0