Energy Storage Market Size, Share | CAGR of 10.3% – Market.us

Global Energy Storage Market Report: Advancing Sustainable Development Goals

Executive Summary

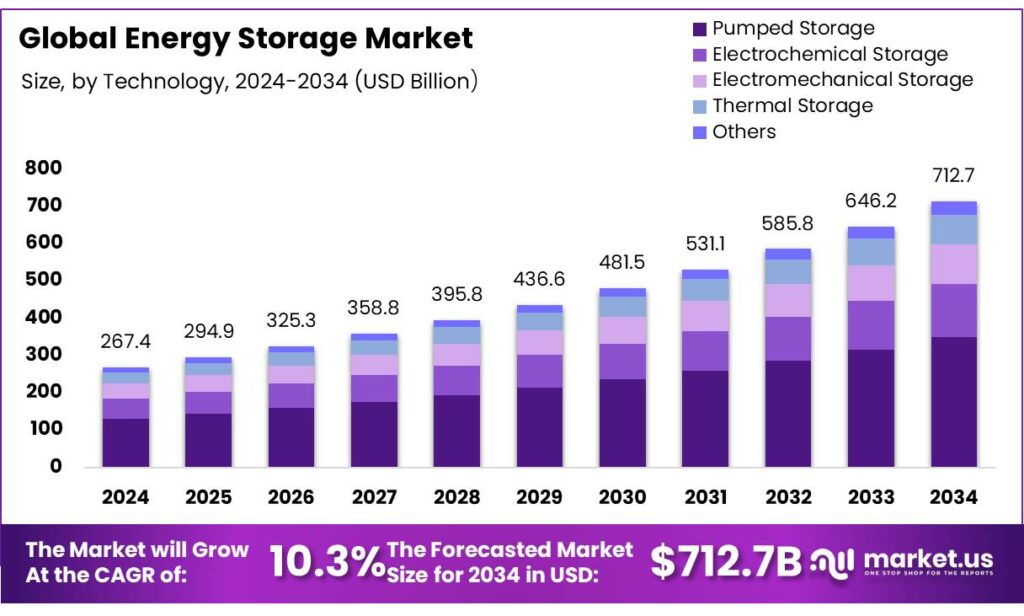

The Global Energy Storage Market is undergoing significant expansion, directly contributing to the achievement of the United Nations Sustainable Development Goals (SDGs), particularly SDG 7 (Affordable and Clean Energy) and SDG 13 (Climate Action). The market is projected to grow from USD 267.4 Billion in 2024 to USD 712.7 Billion by 2034, at a Compound Annual Growth Rate (CAGR) of 10.3%. This growth is instrumental in the global transition to decarbonized power systems by enabling the integration of variable renewable energy sources. In 2024, the Asia-Pacific (APAC) region led this transition, commanding a 47.3% market share valued at USD 126.4 Billion.

Energy storage technologies are fundamental to building resilient infrastructure (SDG 9) and ensuring a stable supply of clean energy. While pumped-storage hydropower remains a dominant technology with approximately 160 GW of capacity, battery storage is expanding rapidly. In 2023, global battery storage capacity increased by 120% to 55.7 GW, underscoring its critical role in supporting higher renewable energy penetration and advancing global climate objectives.

Market Analysis and Contribution to SDGs

Key Market Highlights

- Market Growth Trajectory: The market is forecast to reach USD 712.7 Billion by 2034, reflecting a robust 10.3% CAGR, driven by global commitments to SDG 7 and SDG 13.

- Dominant Technology: Electrochemical Storage technologies represent 48.5% of the market, providing the flexible solutions needed to integrate renewables and modernize energy infrastructure in line with SDG 9.

- Primary Application Sector: The Industrial sector accounts for 51.6% of the market, utilizing energy storage to enhance energy security, improve efficiency, and support sustainable industrialization (SDG 9).

- Regional Leadership: The Asia-Pacific region holds a 47.3% market share (USD 126.4 Billion), leading global efforts in deploying clean energy technologies.

Analysis by Technology

Electrochemical Storage: A Catalyst for SDG 7

In 2024, Electrochemical Storage technologies dominated the market with a 48.5% share. This segment’s leadership is propelled by the widespread adoption of battery systems, which are essential for stabilizing grids and integrating intermittent renewable energy sources such as solar and wind. This technological advancement is a direct enabler of SDG 7, making clean energy more reliable and accessible. Government policies promoting energy transitions and grid stability, particularly in China and the United States, have accelerated the deployment of these systems, reinforcing progress toward national and global climate targets.

Analysis by Application

Industrial Sector: Driving Sustainable Industrialization (SDG 9)

The Industrial segment commanded a 51.6% market share in 2024. This dominance is attributed to increasing investments in large-scale storage systems to manage energy consumption, ensure power reliability, and integrate on-site renewable generation. By adopting these technologies, industries are actively contributing to SDG 9 (Industry, Innovation, and Infrastructure) and SDG 13 (Climate Action). Major industrial economies are leveraging battery energy storage systems (BESS) to reduce grid dependency, lower carbon footprints, and meet corporate sustainability commitments.

Market Dynamics and SDG Alignment

Emerging Trends

Longer-Duration Storage for Enhanced Grid Resilience

A significant market trend is the shift toward longer-duration storage solutions and safer chemistries like Lithium Iron Phosphate (LFP). This evolution is critical for providing sustained power from renewables, thereby ensuring grid stability and supporting the 24/7 availability of clean energy as envisioned by SDG 7. The average installed cost of utility-scale battery storage has declined by approximately 93% since 2010, making multi-hour systems economically viable. Global initiatives, such as the pledge at COP to reach ~1,500 GW of storage by 2030, institutionalize the role of long-duration storage in achieving climate goals.

Market Drivers

Declining Renewable Energy Costs

The primary driver for the energy storage market is the sustained cost reduction of renewable energy. As solar and wind power become cheaper than fossil fuel alternatives, the economic case for storage strengthens. Storage technologies enable the capture and deployment of low-cost renewable electricity, making the energy system more efficient and affordable, which is central to SDG 7. In 2023, 96% of new utility-scale renewable capacity generated electricity at a lower cost than new fossil fuel plants, creating a powerful economic incentive for storage deployment to manage this variable generation.

Market Restraints

Infrastructure Bottlenecks Hindering SDG Progress

A major restraint on market growth is the inadequacy of grid infrastructure, which creates bottlenecks for interconnecting new storage projects. These delays impede the rapid deployment of clean energy solutions, slowing progress toward SDG 7 and SDG 9. The International Energy Agency (IEA) estimates that annual grid investment must nearly double to over USD 600 billion by 2030 to meet climate targets. Overcoming these infrastructure challenges is essential to unlock the full potential of energy storage and accelerate the energy transition.

Market Opportunities

Supporting Sustainable Cities and Infrastructure (SDG 11 & SDG 9)

A key opportunity lies in co-locating energy storage with electric vehicle (EV) fast-charging hubs and data centers. This synergy supports the development of sustainable transportation and resilient digital infrastructure, directly contributing to SDG 11 (Sustainable Cities and Communities) and SDG 9. By managing peak electricity demand from these high-load applications, storage systems can reduce strain on the grid, lower operational costs, and improve service reliability. Government programs, such as the U.S. NEVI program, are funding the build-out of this infrastructure, creating a significant growth vector for distributed energy storage.

Regional Analysis

Asia-Pacific: Leading the Global Energy Transition

The Asia-Pacific region, with a 47.3% market share valued at USD 126.4 Billion in 2024, is at the forefront of the global energy storage market. This leadership is driven by ambitious national policies in countries like China, Japan, South Korea, and India, which are aligned with achieving carbon neutrality and advancing SDG 7. The region’s rapid industrialization and electrification are coupled with large-scale investments in renewable energy and grid modernization, making it a critical hub for the deployment and innovation of energy storage technologies necessary to meet global sustainability targets.

Analysis of Sustainable Development Goals in the Article

1. Which SDGs are addressed or connected to the issues highlighted in the article?

-

SDG 7: Affordable and Clean Energy

The article’s central theme is the growth of the energy storage market, which is crucial for integrating renewable energy sources like solar and wind into the power grid. This directly supports the goal of ensuring access to affordable, reliable, sustainable, and modern energy for all.

-

SDG 9: Industry, Innovation, and Infrastructure

The text discusses the need for significant investment in grid infrastructure to support renewable energy and storage. It also highlights innovation in storage technologies (e.g., new battery chemistries) and the adoption of these technologies by the industrial sector to enhance efficiency and sustainability.

-

SDG 11: Sustainable Cities and Communities

The article mentions the co-location of energy storage with EV fast-charging hubs. This development is key to building sustainable transportation infrastructure within cities, reducing emissions, and improving urban air quality.

-

SDG 13: Climate Action

By enabling the large-scale deployment of renewable energy and facilitating the decarbonization of the power system, energy storage is a critical tool in combating climate change. The article explicitly links storage to “net-zero commitments” and “national climate targets.”

-

SDG 17: Partnerships for the Goals

The article points to several international collaborations and financial partnerships aimed at advancing energy storage, such as the World Bank’s Energy Storage Partnership, the Global Energy Storage & Grids Pledge at COP, and concessional financing for emerging economies.

2. What specific targets under those SDGs can be identified based on the article’s content?

-

SDG 7: Affordable and Clean Energy

- Target 7.2: By 2030, increase substantially the share of renewable energy in the global energy mix. The article emphasizes that energy storage is essential for “balancing variable solar and wind” and enabling “higher variable renewable energy (VRE) penetration.”

- Target 7.a: By 2030, enhance international cooperation to facilitate access to clean energy research and technology… and promote investment in energy infrastructure and clean energy technology. The article mentions the U.S. Department of Energy’s research programs (Long Duration Storage Shot), the World Bank’s financing of storage projects, and its Energy Storage Partnership across 35 countries.

-

SDG 9: Industry, Innovation, and Infrastructure

- Target 9.1: Develop quality, reliable, sustainable and resilient infrastructure… The article highlights the problem of “Grid Interconnection & Transmission Bottlenecks” and cites the IEA’s estimate that “annual grid investment must nearly double to >USD 600 billion by 2030” to build resilient grids.

- Target 9.4: By 2030, upgrade infrastructure and retrofit industries to make them sustainable… with greater adoption of clean and environmentally sound technologies. The article notes that the industrial sector is the largest user of energy storage, adopting it to “manage peak load demands,” integrate renewables, and meet “net-zero commitments.”

-

SDG 11: Sustainable Cities and Communities

- Target 11.2: By 2030, provide access to safe, affordable, accessible and sustainable transport systems for all. The article discusses pairing batteries with public EV fast-charging hubs, supported by programs like the U.S. federal NEVI program, which is crucial for creating sustainable urban transport systems.

-

SDG 13: Climate Action

- Target 13.2: Integrate climate change measures into national policies, strategies and planning. The article references “government-backed energy transition programs,” “national targets for carbon neutrality” in countries like China and India, and the EU’s pledge to reach “~1,500 GW of storage by 2030” as part of its climate strategy.

-

SDG 17: Partnerships for the Goals

- Target 17.7: Promote the development, transfer, dissemination and diffusion of environmentally sound technologies to developing countries. The article mentions the World Bank’s use of “concessional finance to unlock battery storage at scale” in emerging economies.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

-

For Target 7.2 (Increase renewable energy share):

- Installed energy storage capacity: The article provides specific figures, such as “global battery storage capacity grew 120% in 2023 to 55.7 GW” and the U.S. reaching “26 GW” of utility-scale capacity.

- Renewable capacity additions: The article mentions a record “~507 GW of renewable capacity added in 2023.”

-

For Target 7.a (Promote investment and cooperation):

- Financial flows for clean energy: The article cites the World Bank’s financing of “6.3 GWh of battery storage in active projects” and a “US$1 billion global storage initiative” to mobilize more capital.

- Cost reduction of technology: Progress is shown by the “average installed cost of utility-scale battery storage” falling by “~93% since 2010.”

-

For Target 9.1 (Develop resilient infrastructure):

- Annual investment in grids: The article uses the IEA’s benchmark that “annual grid investment must nearly double to >USD 600 billion by 2030.”

- Generation and storage in interconnection queues: The backlog of “~2,300–2,600 GW of generation and storage is waiting in queues” in the U.S. serves as an inverse indicator of progress.

-

For Target 11.2 (Sustainable transport systems):

- Number of public EV charging points: The article states that “more than 1.3 million public charging points were added worldwide” in 2024.

- Public funding for charging infrastructure: The article mentions the “$5 billion” U.S. NEVI program as a measure of government commitment.

-

For Target 13.2 (Integrate climate measures into policy):

- National storage capacity targets: The article mentions the EU’s pledge for “~1,500 GW of storage by 2030” and China’s addition of “over 40 GW of new energy storage capacity” in 2024 as evidence of policy implementation.

4. Summary Table of SDGs, Targets, and Indicators

| SDGs | Targets | Indicators |

|---|---|---|

| SDG 7: Affordable and Clean Energy |

7.2: Increase substantially the share of renewable energy in the global energy mix.

7.a: Enhance international cooperation and promote investment in clean energy technology and infrastructure. |

– Installed capacity of energy storage (e.g., global battery capacity at 55.7 GW in 2023). – Annual renewable capacity additions (e.g., ~507 GW in 2023). – International financial flows for storage projects (e.g., World Bank’s US$1 billion initiative). – Reduction in technology cost (e.g., battery storage costs fell ~93% since 2010). |

| SDG 9: Industry, Innovation, and Infrastructure |

9.1: Develop quality, reliable, sustainable and resilient infrastructure.

9.4: Upgrade infrastructure and retrofit industries to make them sustainable. |

– Annual investment in grid infrastructure (target of >USD 600 billion by 2030). – Volume of projects in interconnection queues (~2,300–2,600 GW in the U.S.). – Market share of energy storage adoption by the industrial sector (51.6%). |

| SDG 11: Sustainable Cities and Communities | 11.2: Provide access to sustainable transport systems for all. |

– Number of public EV charging points added annually (1.3 million in 2024). – Amount of public funding allocated to EV infrastructure (e.g., $5 billion from U.S. NEVI program). |

| SDG 13: Climate Action | 13.2: Integrate climate change measures into national policies, strategies and planning. |

– National and regional targets for energy storage capacity (e.g., EU’s ~1,500 GW by 2030). – Implementation of national energy storage missions and policies. |

| SDG 17: Partnerships for the Goals | 17.7: Promote the transfer and diffusion of environmentally sound technologies to developing countries. |

– Amount of concessional finance available for storage in emerging economies. – Number of countries participating in international partnerships (e.g., 35 countries in the World Bank’s Energy Storage Partnership). |

Source: market.us

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0