Power Generation Equipment Market Size, Share | CAGR of 5.1% – Market.us

Report on the Global Power Generation Equipment Market and its Contribution to Sustainable Development Goals (SDGs)

Executive Summary

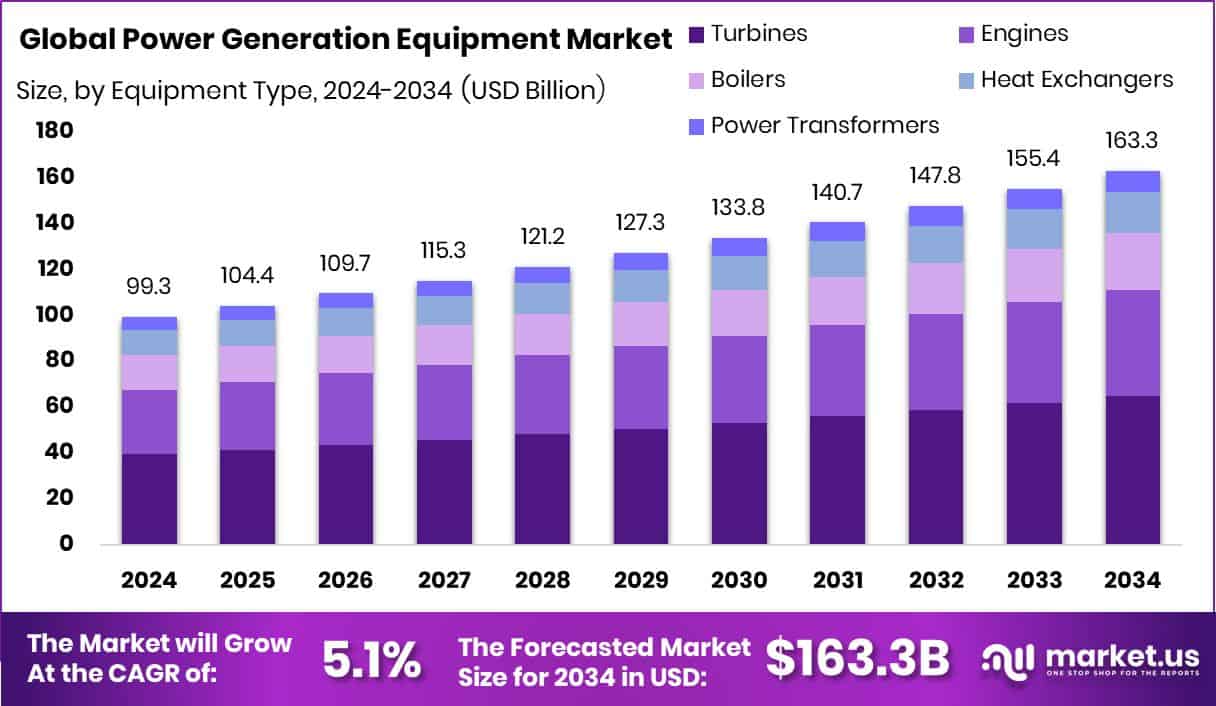

The Global Power Generation Equipment Market is projected to expand from USD 99.3 billion in 2024 to USD 163.3 billion by 2034, growing at a Compound Annual Growth Rate (CAGR) of 5.1%. This growth is intrinsically linked to the global pursuit of the United Nations Sustainable Development Goals, particularly SDG 7 (Affordable and Clean Energy) and SDG 9 (Industry, Innovation, and Infrastructure). The market encompasses machinery essential for converting energy sources into electricity, including turbines, generators, and control systems. The global transition towards cleaner and more resilient energy systems, driven by decarbonization policies and the need for energy security, is a primary catalyst for market expansion. The Asia-Pacific region, with a 47.30% market share, is central to this transformation, spearheading large-scale electrification and renewable energy projects.

Market Segmentation Analysis: A Perspective on SDG Alignment

Equipment Type Analysis

Turbines represent the dominant equipment segment, holding a 39.8% market share. Their critical role in both renewable (wind, hydro) and conventional power systems underscores their importance in the global energy transition. The continued installation and modernization of turbine systems are fundamental to increasing the share of renewable energy in the global energy mix, directly supporting the objectives of SDG 7.

Fuel Source Analysis

Fossil fuels currently command a 56.9% share of the market, reflecting the legacy of existing infrastructure and the need for stable baseload power. This dominance highlights the significant challenge in achieving SDG 13 (Climate Action). However, the market’s trajectory indicates a progressive shift, with growing investments in renewable energy equipment signaling a long-term commitment to decarbonization.

Capacity Range Analysis

Medium-capacity systems (5–50 MW) lead the market with a 44.3% share. These systems are vital for industrial facilities and distributed power networks, which enhance energy resilience and access in urban and remote communities. This contributes to SDG 11 (Sustainable Cities and Communities) by providing flexible and scalable power solutions.

Application Analysis

Baseload generation accounts for 41.2% of the market, providing the continuous, reliable electricity supply necessary for stable economies and public services. This reliability is a cornerstone of sustainable industrialization and resilient infrastructure, as outlined in SDG 9.

End-Use Analysis

The utility sector is the largest end-user, with a 49.7% market share. Utilities are at the forefront of implementing national energy strategies and large-scale infrastructure projects. Their investment decisions are pivotal in steering the global energy system towards the targets of SDG 7 and SDG 13.

Market Dynamics and their Impact on Sustainable Development

Driving Factors: Policy and Investment as Catalysts for SDG 7 and SDG 9

Government policies and substantial financial investments are accelerating the adoption of sustainable energy technologies. These drivers are crucial for building modern and resilient energy infrastructure. Examples include:

- The UK’s $720 million incentive for wind farm development.

- A $20 million U.S. Department of Energy initiative for wind technology recycling, promoting circular economy principles aligned with SDG 12 (Responsible Consumption and Production).

- Significant capital injections into next-generation turbine and hybrid power systems.

Restraining Factors: Economic Barriers to Universal Energy Access

The high upfront cost of power generation equipment remains a significant barrier, particularly for developing economies. This financial constraint impedes progress toward universal energy access as mandated by SDG 7. While initiatives like Mission 300 aim to bridge this gap in Africa, the disparity between available funding and deployment needs slows the transition to cleaner, more efficient energy systems.

Growth Opportunities: Renewable Projects Advancing Climate Action (SDG 13)

The proliferation of renewable energy projects presents a major growth opportunity. These initiatives directly address climate change and create demand for advanced power generation equipment. Key developments include:

- A PHP 60-million funding facility in the Philippines to expand renewable-powered telecom solutions, improving infrastructure in off-grid areas.

- Over €2 billion from the European Investment Bank for renewable energy projects in Africa, accelerating solar and wind development.

Latest Trends: The Shift Towards Smart and Resilient Energy Infrastructure (SDG 9)

A dominant market trend is the integration of smart technologies with renewable energy systems. This shift is creating more efficient, automated, and resilient power grids. Large-scale funding programs, such as the proposed $6 billion grid modernization plan by Türkiye and the World Bank, exemplify this move towards the sustainable infrastructure required to meet future energy demands.

Regional Analysis: Progress Towards Global Energy and Climate Goals

Asia-Pacific

Holding a 47.30% market share valued at USD 46.9 billion, the Asia-Pacific region is a critical driver of global energy development. Rapid industrialization and urbanization fuel the demand for new power infrastructure, making the region’s transition to sustainable energy pivotal for achieving global targets under SDG 7, SDG 8 (Decent Work and Economic Growth), and SDG 9.

North America and Europe

These regions are focused on modernizing aging energy assets and enhancing system efficiency. Their efforts to upgrade grids and integrate advanced generation solutions contribute to long-term energy security and align with SDG 12 by promoting more sustainable production patterns.

Middle East, Africa, and Latin America

Increased equipment installation in these regions is essential for expanding electrification and supporting industrial growth. These efforts are fundamental to achieving universal energy access (SDG 7) and fostering economic development through improved infrastructure (SDG 9).

Key Stakeholder Contributions and Recent Developments

Analysis of Key Players

Market leaders are instrumental in advancing sustainable energy solutions. Their contributions include:

- ABB: Focuses on automation and grid stability, enabling the integration of renewable energy sources.

- Bharat Heavy Electricals Limited: Supplies large-scale equipment for baseload power, ensuring the grid reliability needed to support economic activity.

- Briggs & Stratton: Provides distributed and smaller-scale power systems, enhancing energy access and resilience at the community level.

Recent Developments Aligned with SDGs

- December 2024: ABB’s acquisition of Gamesa Electric’s power electronics business enhances its portfolio in renewable energy conversion technologies, directly supporting the advancement of SDG 7.

- February 2024: Briggs & Stratton’s subsidiary, Allmand, launched a hybrid light tower that reduces emissions and fuel consumption, demonstrating innovation in sustainable production and climate action (SDG 12 and SDG 13).

Analysis of Sustainable Development Goals in the Power Generation Equipment Market Article

1. Which SDGs are addressed or connected to the issues highlighted in the article?

The article on the Power Generation Equipment Market highlights issues and trends that are directly connected to several Sustainable Development Goals (SDGs). The analysis reveals connections to the following goals:

- SDG 7: Affordable and Clean Energy – The core subject of the article is power generation. It discusses the global shift towards “cleaner, more efficient, and more resilient energy systems,” the growth of “renewable projects” (wind, hydro, solar), and efforts towards “growing electrification,” especially in developing regions like Asia-Pacific and Africa.

- SDG 9: Industry, Innovation, and Infrastructure – The article emphasizes the importance of infrastructure development, such as “grid expansion,” “modernisation of old power plants,” and building “resilient energy systems.” It also points to innovation through “next-generation technology,” “smart renewable expansion,” and “digital control systems.”

- SDG 8: Decent Work and Economic Growth – The projected growth of the market from “USD 99.3 billion in 2024” to “USD 163.3 billion by 2034” at a “CAGR of 5.1%” signifies substantial economic activity. Investments in new technologies and infrastructure projects create jobs and drive economic growth.

- SDG 13: Climate Action – The trend towards renewable energy and “decarbonization” is a central theme. The article notes that nations are shifting to “cleaner power” to reduce emissions, as exemplified by developments like the “Hybrid LT-Series’ light tower” which reduces emissions and fuel use.

- SDG 17: Partnerships for the Goals – The article provides multiple examples of international cooperation and financial partnerships aimed at advancing energy goals. It mentions large-scale funding from institutions like the “World Bank,” the “European Investment Bank,” and the “Asian Development Bank (ADB)” to support renewable energy and grid modernization in various countries.

2. What specific targets under those SDGs can be identified based on the article’s content?

Based on the article’s content, several specific SDG targets can be identified:

-

SDG 7: Affordable and Clean Energy

- Target 7.1: By 2030, ensure universal access to affordable, reliable and modern energy services. This is addressed through the discussion of “growing electrification” and initiatives like “Mission 300 raising billions to power millions of Africans with renewable energy.”

- Target 7.2: By 2030, increase substantially the share of renewable energy in the global energy mix. This is a central theme, highlighted by the “rising wave of renewable energy projects,” investments in “wind farm incentives,” and the growth of solar, wind, and hybrid power systems.

- Target 7.a: By 2030, enhance international cooperation to facilitate access to clean energy research and technology. The article explicitly mentions this through examples of international funding, such as “Africa is set to receive over €2 billion from the European Investment Bank for renewable energy projects” and “Türkiye and the World Bank prepare a $6 billion grid funding program for renewable integration.”

-

SDG 9: Industry, Innovation, and Infrastructure

- Target 9.1: Develop quality, reliable, sustainable and resilient infrastructure. This is reflected in the focus on “grid expansion,” “modernisation of old power plants,” and building “resilient energy systems” to ensure “grid stability” and “uninterrupted electricity supply.”

- Target 9.4: By 2030, upgrade infrastructure and retrofit industries to make them sustainable. The article discusses the “modernisation of older plants, where efficiency upgrades and replacement of legacy turbine systems are common” and the shift towards “cleaner, more efficient” systems.

-

SDG 13: Climate Action

- Target 13.2: Integrate climate change measures into national policies, strategies and planning. This is shown through “government-backed clean-energy programs” and “policy activity happening around energy infrastructure” that are driving the market towards renewable solutions.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

The article provides both direct and implied indicators that can be used to measure progress towards the identified SDG targets:

-

Indicators for SDG 7

- Indicator 7.2.1 (Renewable energy share in the total final energy consumption): While the article states that fossil fuels still hold a dominant “56.9% share,” the clear trend and massive investments in renewables imply a measurable shift. The growth of renewable projects is a key “growth opportunity” mentioned.

- Indicator 7.a.1 (International financial flows to developing countries in support of clean energy): The article provides specific financial figures that serve as direct indicators. Examples include:

- “€2 billion from the European Investment Bank” for renewable projects in Africa.

- A “$6 billion grid funding program” from the World Bank for Türkiye.

- “$331 million in funding from ADB” for a renewable energy project in India.

- “PHP 60-million funding facility” in the Philippines.

-

Indicators for SDG 9

- Market Growth and Investment: The overall market growth from “USD 99.3 billion” to “USD 163.3 billion” and the specific investments mentioned (e.g., Britain’s “$720 million” for wind farm incentives) serve as a proxy indicator for investment in sustainable infrastructure.

- Adoption of Efficient Technology: The market share of advanced equipment like turbines (“39.8%”) and the trend towards “smarter and renewable-focused energy systems” can be used to measure the upgrading of infrastructure (Target 9.4).

-

Indicators for SDG 13

- Investment in Clean Energy: The financial commitments to renewable energy projects (as listed under SDG 7) are also direct indicators of financial resources being mobilized to implement climate action policies.

- Policy Implementation: The mention of “government-backed clean-energy programs” and “policy support” that “accelerates adoption” of renewables indicates progress in integrating climate measures into national planning.

4. Summary Table of SDGs, Targets, and Indicators

| SDGs | Targets | Indicators Identified in the Article |

|---|---|---|

| SDG 7: Affordable and Clean Energy |

7.1: Ensure universal access to affordable, reliable and modern energy services. 7.2: Increase substantially the share of renewable energy. 7.a: Enhance international cooperation and investment in clean energy. |

– Mention of “growing electrification” and projects to “power millions of Africans.” – Growth in “renewable projects” (wind, hydro, solar) despite fossil fuels’ current 56.9% market share. – Specific financial flows mentioned: €2 billion (EIB for Africa), $6 billion (World Bank for Türkiye), $331 million (ADB for India). |

| SDG 9: Industry, Innovation, and Infrastructure |

9.1: Develop quality, reliable, sustainable and resilient infrastructure. 9.4: Upgrade infrastructure and retrofit industries for sustainability. |

– Focus on “grid expansion,” “grid stability,” and building “resilient energy systems.” – Trend of “modernisation of old power plants” with “efficiency upgrades” and replacement of legacy systems. |

| SDG 13: Climate Action | 13.2: Integrate climate change measures into national policies and planning. |

– “Government-backed clean-energy programs” and “policy activity” driving the shift to renewables. – National strategies focused on “decarbonization” and adopting “cleaner power systems.” |

| SDG 8: Decent Work and Economic Growth | 8.2: Achieve higher levels of economic productivity through technological upgrading and innovation. |

– Projected market growth at a “CAGR of 5.1%” from $99.3 billion to $163.3 billion. – Investment in “next-generation technology” and “innovation” driving the market. |

| SDG 17: Partnerships for the Goals | 17.3: Mobilize financial resources for developing countries from multiple sources. | – Explicit examples of multilateral funding from the “World Bank,” “European Investment Bank,” and “Asian Development Bank (ADB)” for energy projects in developing regions. |

Source: market.us

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0