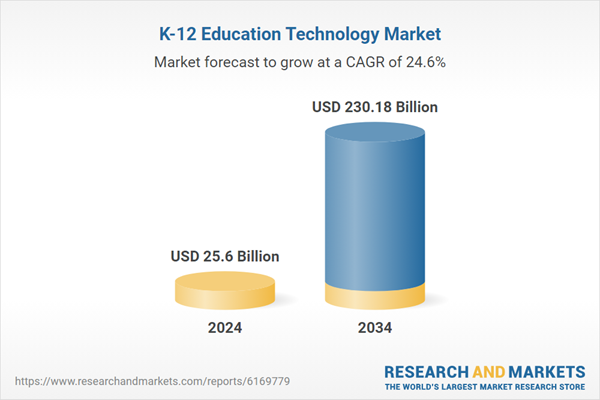

$230+ Bn K-12 Education Technology Global Market Opportunities and Strategies to 2034 – GlobeNewswire

Global K-12 Education Technology Market Report: Advancing Sustainable Development Goal 4

This report analyzes the global K-12 education technology market, focusing on its role in achieving Sustainable Development Goal 4 (SDG 4), which aims to ensure inclusive and equitable quality education and promote lifelong learning opportunities for all. The market’s expansion reflects a global commitment to leveraging technology to enhance educational access, quality, and outcomes.

Market Performance and Projections

Historic and Forecasted Growth

The global K-12 education technology market is demonstrating significant growth, underscoring its importance in building resilient and modern education systems aligned with SDG 4.

- The market reached a value of approximately $25.6 billion in 2024, following a compound annual growth rate (CAGR) of 25.77% from 2019.

- Projections indicate the market will expand to $77.25 billion in 2029 at a CAGR of 24.72%.

- Further growth is anticipated, with the market expected to reach $230.18 billion in 2034, growing at a CAGR of 24.40% from 2029.

Growth Dynamics and Alignment with SDGs

Key Market Drivers

Growth is propelled by factors that directly support the targets of SDG 4 and other related goals.

- Rising Digital Adoption in Classrooms: Enhances learning environments and provides access to a wider range of educational resources, contributing to SDG Target 4.a to build and upgrade education facilities.

- Demand for Remote and Hybrid Learning: Expands access to education for all, a core principle of SDG 4, ensuring learning continuity during disruptions.

- Favorable Government Initiatives: Public investment in EdTech infrastructure supports national strategies to achieve quality education and reduce inequalities (SDG 10).

- Integration of AI and Machine Learning: Enables personalized learning pathways, helping to meet the diverse needs of all learners and improve learning outcomes (SDG Target 4.1).

- Gamified Learning Platforms: Increases student engagement and makes learning more inclusive and effective, fostering a positive educational experience.

Market Restraints and SDG Challenges

Certain challenges hinder the universal application of EdTech, posing risks to the achievement of inclusive education goals.

- Digital Divide and Accessibility Issues: This remains a primary barrier to equitable access, directly conflicting with SDG 4 and SDG 10 (Reduced Inequalities) by marginalizing students in underserved communities.

- Privacy and Security Challenges: Ensuring safe and secure digital learning environments is crucial for student well-being and is an integral part of providing quality education.

- High Implementation and Maintenance Costs: Financial barriers can widen the gap between well-resourced and under-funded institutions, exacerbating educational inequalities.

- Resistance to Change: A lack of training and support for educators can limit the effective integration of technology to improve teaching and learning outcomes.

Regional Analysis: Bridging Global Education Gaps

Market Leadership and Distribution

In 2024, North America was the largest region in the K-12 education technology market, accounting for 32.80% of the total, valued at $8.39 billion. It was followed by Asia Pacific and Western Europe.

Emerging Growth and SDG Impact

The fastest-growing regions are critical areas for leveraging EdTech to accelerate progress towards SDG 4.

- Asia Pacific: Forecasted to grow at a CAGR of 27.94%.

- Africa: Forecasted to grow at a CAGR of 25.15%.

Growth in these regions signifies a crucial opportunity to use technology to overcome long-standing educational barriers and provide quality learning opportunities to millions of children.

Market Segmentation Analysis

By Type

The market is segmented into hardware, solution, software, and support. The hardware segment was the largest in 2024 at $10.09 billion. However, the solution segment is projected to be the fastest-growing, indicating a shift towards integrated systems that support comprehensive educational needs.

By Technology

Key technologies include educational gaming, analytics, ERP, security, and dashboards. Educational gaming was the largest segment in 2024 at $6.25 billion and is expected to remain the fastest-growing. This trend supports SDG 4 by promoting more engaging and effective learning methods.

By Application

The market is divided into online and offline applications. The online segment is dominant, accounting for $19.89 billion in 2024, and is projected to be the fastest-growing. This reflects the global trend towards digital platforms to ensure education is accessible and flexible.

By Downstream Industry

Segments include pre-primary, primary, middle, and high school. The primary school segment was the largest in 2024 at $7.77 billion and is expected to be the fastest-growing. Focusing technology on foundational learning is critical for achieving lifelong educational success as envisioned by SDG 4.

Competitive Landscape

Market Concentration

The global K-12 education technology market is fairly fragmented. In 2023, the top ten competitors accounted for 21.68% of the total market.

Leading Competitors

- Pearson Education Inc. (5.43%)

- Mcgraw-hill Education (3.27%)

- Cengage Learning Pvt. Ltd. (2.46%)

- Stride Learning Inc. (2.34%)

- TAL Education Group (2.19%)

- BlackBoard Inc. (1.56%)

- Amazon Web Services (AWS) for Education (1.48%)

- Microsoft Education (1.27%)

- Byju’s (Think and Learn Pvt. Ltd.) (0.85%)

- International Business Machines (IBM) Corporation (0.82%)

Strategic Outlook and Future Trends for Achieving SDG 4

Market strategies are increasingly focused on innovations that align with the goals of quality, equity, and inclusion in education.

Market-Trend-Based Strategies

- AI-Powered Personalization: Developing platforms that adapt to individual learning paces and styles to ensure no student is left behind, directly supporting SDG 4’s equity agenda.

- Immersive STEM Programs: Using technology to provide hands-on learning experiences in science, technology, engineering, and math, preparing students for the industries of the future (SDG 9).

- Integrated SaaS Platforms: Creating solutions that streamline administration and teaching workflows, allowing educators to focus more on instructional quality.

- Focus on Digital Resources: Enhancing access to high-quality digital content and tools to create immersive and effective learning experiences for all students.

Analysis of Sustainable Development Goals in the K-12 Education Technology Market Article

1. Which SDGs are addressed or connected to the issues highlighted in the article?

-

SDG 4: Quality Education

- The entire article is centered on the K-12 education technology market, which directly supports the goal of ensuring inclusive and equitable quality education. It discusses tools like “AI and machine learning,” “gamified learning platforms,” and “remote and hybrid learning” solutions, all of which are aimed at enhancing the quality and delivery of education for students in pre-primary through high school.

-

SDG 9: Industry, Innovation, and Infrastructure

- The article details the growth and innovation within the edtech industry. It highlights the development of new technologies (“AI-driven innovation,” “cloud-based solutions”) and the infrastructure required for their implementation (“digital adoption in classrooms”). The market’s projected growth to “$230.18 billion in 2034” signifies a major industrial and innovative effort.

-

SDG 10: Reduced Inequalities

- The article explicitly mentions “digital divide and accessibility issues” as a factor that negatively affected growth. This directly addresses the challenge of inequality in access to educational resources and technology, which is a core concern of SDG 10. The report’s note that the fastest-growing regions will be “Asia Pacific and Africa” also points towards efforts to bridge the global educational gap.

-

SDG 17: Partnerships for the Goals

- The article points to the importance of collaboration to achieve market growth. It mentions “favorable government initiatives” driving growth and notes that a key player strategy is to strengthen business “through partnerships.” This reflects the multi-stakeholder approach (public-private partnerships) essential for achieving the SDGs.

2. What specific targets under those SDGs can be identified based on the article’s content?

-

Target 4.1: By 2030, ensure that all girls and boys complete free, equitable and quality primary and secondary education.

- The article’s focus is on the “K-12 education technology market,” which covers primary and secondary schooling. The development of technologies like “personalized learning” platforms and “AI-powered solutions” aims to improve the quality and effectiveness of education for all students within this range.

-

Target 4.a: Build and upgrade education facilities that are child, disability and gender sensitive and provide safe, non-violent, inclusive and effective learning environments for all.

- The massive investment in education technology, including “hardware,” “software,” and “cloud-based solutions,” represents a significant upgrade of educational facilities into modern, digital learning environments. The mention of “accessibility issues” as a challenge directly relates to the need for inclusive learning environments.

-

Target 9.c: Significantly increase access to information and communications technology (ICT) and strive to provide universal and affordable access to the Internet.

- The article’s data shows that the “online” segment of the market is the largest, accounting for “77.70% or $19.89 billion” in 2024. This demonstrates a massive increase in the use of and access to ICT for educational purposes. The growth of remote and hybrid learning models is entirely dependent on this target.

-

Target 10.2: By 2030, empower and promote the social and economic inclusion of all.

- The article identifies the “digital divide” as a key challenge. Overcoming this divide through the deployment of education technology, especially in fast-growing regions like “Africa,” is crucial for ensuring that all children have the educational opportunities necessary for social and economic inclusion.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

-

Implied Indicator for Target 4.a: The overall market value and its growth can serve as a proxy indicator for the upgrading of education facilities with technology.

- The article states the market reached “$25.6 billion in 2024” and is forecast to reach “$230.18 billion in 2034.” This financial data implies a significant and growing proportion of educational infrastructure is being enhanced with technology.

-

Implied Indicator for Target 9.c: The market share of online vs. offline educational applications serves as an indicator for access to and use of ICT in education.

- The article provides a specific metric: the “online market was the largest segment… accounting for 77.70%.” The projected growth of this segment to gain “$41.88 billion of global annual sales by 2029” can be used to track the increasing penetration of ICT in the education sector.

-

Implied Indicator for Target 10.2: Regional market growth rates can be used as a proxy for efforts to reduce the global digital divide in education.

- The report highlights that the “fastest-growing regions… will be Asia Pacific and Africa” with CAGRs of “27.94% and 25.15% respectively.” Tracking this accelerated growth in developing regions can indicate progress in closing the educational technology gap with more developed regions like North America.

4. Table of SDGs, Targets, and Indicators

| SDGs | Targets | Indicators (Mentioned or Implied in the Article) |

|---|---|---|

| SDG 4: Quality Education | Target 4.a: Build and upgrade education facilities… and provide… inclusive and effective learning environments for all. | The total market value of K-12 education technology, growing from $25.6 billion in 2024 to a forecasted $230.18 billion in 2034, serves as a proxy for investment in upgrading educational facilities with technology. |

| SDG 9: Industry, Innovation, and Infrastructure | Target 9.c: Significantly increase access to information and communications technology (ICT). | The market share of the “online” applications segment, which accounted for 77.70% ($19.89 billion) of the market in 2024, indicates the level of ICT integration in education. |

| SDG 10: Reduced Inequalities | Target 10.2: Empower and promote the social and economic inclusion of all. | The comparative regional growth rates, with Asia Pacific (27.94%) and Africa (25.15%) being the fastest-growing, imply an effort to reduce the global “digital divide” in educational technology access. |

| SDG 17: Partnerships for the Goals | Target 17.17: Encourage and promote effective public, public-private and civil society partnerships. | The article’s mention of “favorable government initiatives” and corporate strategies focused on “partnerships” implies the formation of public-private collaborations to advance educational goals. |

Source: globenewswire.com

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0