Photovoltaic (PV) Battery Market Size, Share | CAGR of 11.5% – Market.us

Report on the Global Photovoltaic (PV) Battery Market and its Contribution to Sustainable Development Goals

This report provides an analysis of the Global Photovoltaic (PV) Battery Market, examining its growth, key segments, and drivers through the lens of the United Nations Sustainable Development Goals (SDGs). The market is a critical enabler for achieving global targets related to clean energy, climate action, and sustainable infrastructure.

Market Overview and Alignment with SDG 7 and SDG 13

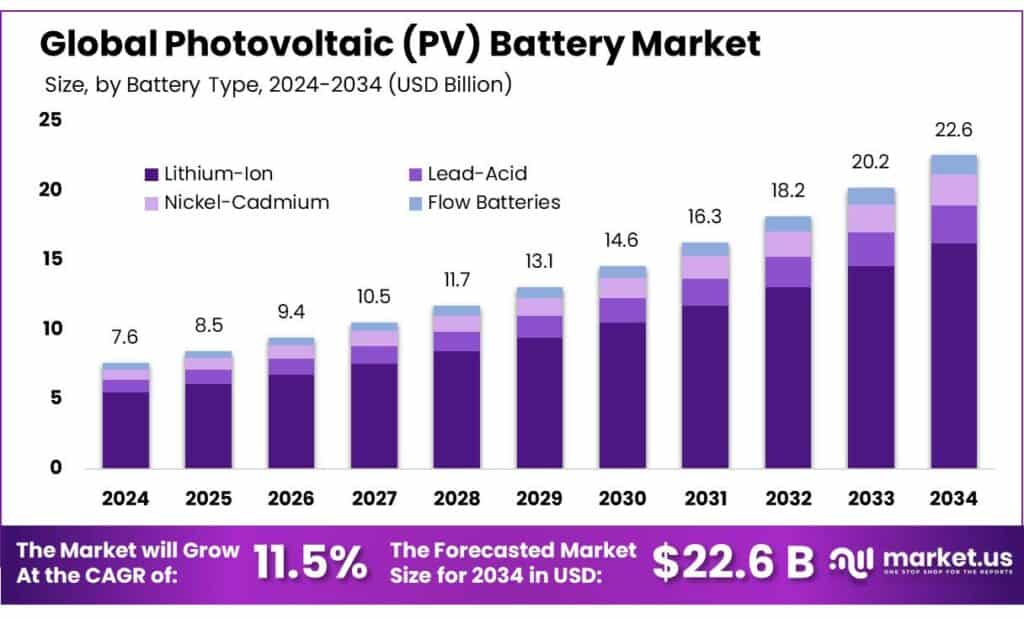

The Global Photovoltaic (PV) Battery Market is projected to expand from USD 7.6 Billion in 2024 to USD 22.6 Billion by 2034, reflecting a Compound Annual Growth Rate (CAGR) of 11.5%. This growth is intrinsically linked to the advancement of SDG 7 (Affordable and Clean Energy) by enhancing the reliability and accessibility of solar power. PV batteries, which store electricity from solar panels for later use, are essential for stabilizing grids, providing backup power, and ensuring a consistent energy supply, thereby accelerating the transition from fossil fuels and directly supporting SDG 13 (Climate Action).

The industrial context underscores this trend. In 2023, a record 407 GW of new solar PV capacity was installed globally, bringing the total to approximately 1.6 TW. Concurrently, global battery storage capacity grew by 120% to 55.7 GW, illustrating the synergistic scaling of technologies required for a sustainable energy future. North America demonstrated significant leadership in 2024, commanding a 38.9% market share valued at USD 2.9 billion, highlighting regional commitment to building resilient and clean energy infrastructure in line with SDG 9 (Industry, Innovation, and Infrastructure).

Key Market Highlights in the Context of Sustainable Development

- Market Growth: A projected increase to USD 22.6 Billion by 2034 at an 11.5% CAGR signifies a robust investment in infrastructure critical for SDG 7.

- Dominant Technology (Lithium-Ion): Holding over 72.4% of the market, lithium-ion technology’s efficiency is pivotal for deploying effective clean energy solutions.

- Dominant Chemistry (Lithium Cobalt Oxide): With a 56.9% share, this chemistry’s high energy density supports compact energy storage, crucial for residential and urban applications under SDG 11 (Sustainable Cities and Communities).

- Key Storage Capacity (5-10 kWh): This segment’s 39.5% market share reflects its suitability for residential use, empowering households to participate in the energy transition.

- Leading Application (Residential): The residential sector’s 44.8% share underscores a growing movement towards decentralized, resilient energy systems that enhance community sustainability (SDG 11).

- Regional Leadership (North America): With a 38.9% share, the region’s progress is driven by policies that actively promote climate action and clean energy adoption.

Market Segmentation Analysis

Analysis by Battery Type: Lithium-Ion’s Role in Energy Transition

In 2024, Lithium-Ion batteries dominated the market with a 72.4% share. This leadership is due to superior energy density, longer cycle life, and declining costs, making it the most viable technology for advancing SDG 7. Its widespread adoption across residential, commercial, and utility-scale projects enables the firming of variable solar output, a necessary step for integrating renewables into the grid and reducing carbon emissions as targeted by SDG 13.

Analysis by Chemistry: Lithium Cobalt Oxide and Performance

Lithium Cobalt Oxide chemistry accounted for 56.9% of the market in 2024. Its high energy density allows for more compact and lightweight battery packs, facilitating installations in space-constrained urban environments and contributing to the development of sustainable cities and communities (SDG 11). As the market matures, lifecycle management and recycling become critical for ensuring this technology aligns with SDG 12 (Responsible Consumption and Production).

Analysis by Storage Capacity: Empowering Consumers

The 5–10 kWh capacity segment held a 39.5% market share in 2024, primarily serving the residential sector. This capacity range provides an optimal balance of energy storage for daily use and backup power, empowering homeowners with energy independence and lower electricity bills. This trend supports the decentralization of energy systems, a key component of building resilient and sustainable communities (SDG 11).

Analysis by Application: Residential Sector Leading the Charge

The residential sector was the largest application segment with a 44.8% share in 2024. This demand is driven by a desire for energy resilience and cost savings, directly supporting household-level adoption of clean energy (SDG 7). This behind-the-meter storage growth is fundamental to creating flexible and stable grids capable of handling high shares of renewable energy.

Key Market Segments

By Battery Type

- Lithium-Ion

- Lead-Acid

- Nickel-Cadmium

- Flow Batteries

By Chemistry

- Lithium Cobalt Oxide

- Lithium Iron Phosphate

- Nickel Manganese Cobalt

By Storage Capacity

- Below 5 kWh

- 5-10 kWh

- 10-15 kWh

- Above 15 kWh

By Application

- Residential

- Commercial

- Industrial

- Utility Scale

Emerging Trends: Supporting SDG 2 (Zero Hunger)

Solar-Powered Cold Chains: A New Frontier for PV Batteries

A significant trend is the application of PV batteries in food and agriculture cold chains. This innovation directly addresses SDG 2 (Zero Hunger) by reducing post-harvest food loss. The Food and Agriculture Organization (FAO) reports that 13.3% of food is lost globally after harvest. PV-powered cold storage offers a reliable solution in regions with weak or non-existent grids, preventing the spoilage of perishable goods like dairy, fish, fruits, and vegetables. This application transforms PV batteries from a power-sector tool into a critical component of sustainable food systems, reducing food waste and improving farmer incomes, thereby contributing to SDG 12.

Market Dynamics

Drivers: Accelerating Progress on SDG 7 and SDG 13

The market is primarily driven by the rapid global expansion of solar power and a dramatic reduction in battery costs. The International Renewable Energy Agency (IRENA) notes that battery storage project costs fell by 93% between 2010 and 2024. This cost deflation, coupled with supportive government policies like the U.S. Inflation Reduction Act, makes solar-plus-storage systems economically viable. These drivers are accelerating the deployment of clean energy infrastructure, which is essential for meeting the targets of SDG 7 and SDG 13.

Restraints: Challenges to SDG 12 (Responsible Consumption and Production)

Market growth is constrained by supply chain vulnerabilities for critical raw materials like lithium and cobalt, and inadequate recycling infrastructure. The International Energy Agency (IEA) projects that lithium demand will increase by over 3.5 times by 2030. The current low recycling rates (less than 20% for lithium-ion batteries) pose a significant challenge to achieving a circular economy. Addressing these issues is crucial for aligning the industry’s growth with the principles of SDG 12.

Opportunities: Advancing SDG 1 (No Poverty) and SDG 2 (Zero Hunger)

A major opportunity lies in rural electrification, particularly in off-grid areas. Approximately 685 million people lacked electricity access in 2022. PV battery systems can power rural homes, clinics, and businesses, creating economic opportunities and improving quality of life (SDG 1 and SDG 8). Furthermore, their use in powering irrigation and cold storage for agriculture enhances food security and builds climate-resilient food systems, directly supporting SDG 2.

Regional Insights

In 2024, North America led the market with a 38.90% share, valued at USD 2.9 billion. This dominance is a result of mature policy frameworks, significant utility-scale procurements, and strong consumer demand for resilient energy solutions. The region’s progress in deploying solar-plus-storage systems serves as a model for developing the sustainable infrastructure needed to achieve SDG 7, SDG 9, and SDG 11 on a larger scale.

Key Regions and Countries

- North America

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players and Industry Developments

Leading companies are driving innovation (SDG 9) and expanding the market’s reach. Recent developments, such as SolarEdge Technologies’ introduction of a home battery with domestic-content incentives and SunPower’s return to profitability, highlight the industry’s dynamic nature and its continuous contribution to the clean energy transition.

Top Key Players

- Q CELLS

- SolarEdge Technologies

- JinkoSolar

- SunPower

- CATL

- Longi Green Energy

- Enphase Energy

- Panasonic

- Trina Solar

- BYD

Analysis of Sustainable Development Goals (SDGs) in the Article

1. Which SDGs are addressed or connected to the issues highlighted in the article?

-

SDG 7: Affordable and Clean Energy

- The entire article is centered on photovoltaic (PV) batteries, which are a key technology for storing solar energy. This directly relates to increasing the share of renewable energy in the global energy mix and ensuring access to reliable electricity. The text discusses the rapid growth of solar PV capacity, the falling costs of battery storage, and the role of PV-battery systems in providing power, especially in areas with weak or no grid access.

-

SDG 2: Zero Hunger

- The article highlights the emerging trend of using PV batteries to power sustainable cold chains for food and agriculture. It explicitly mentions that this technology helps reduce post-harvest food loss, which is a major contributor to food insecurity. The text cites FAO data on food loss and explains how solar-powered cold rooms can preserve perishable goods like milk, fruit, and fish, thereby strengthening food systems.

-

SDG 13: Climate Action

- The article connects the adoption of PV batteries to climate goals. It mentions that these systems are crucial for integrating variable renewables like solar into the grid, which is essential for meeting net-zero targets and reducing greenhouse gas emissions. The text also points out that solar-powered irrigation can cut emissions from water pumping by up to 95% compared to diesel alternatives.

-

SDG 9: Industry, Innovation, and Infrastructure

- The report details the significant industrial growth, technological innovation, and infrastructure development within the PV battery market. It discusses the scaling of manufacturing, cost reductions through technological improvements, and the deployment of both distributed (residential) and utility-scale storage infrastructure. This aligns with building resilient infrastructure and promoting sustainable industrialization.

-

SDG 12: Responsible Consumption and Production

- The “Restraints” section directly addresses issues of sustainable production by discussing the reliance on critical raw materials like lithium and cobalt. It highlights the challenges in supply chains and the urgent need for better recycling systems for end-of-life batteries, which is a core component of ensuring sustainable consumption and production patterns.

-

SDG 1: No Poverty

- The article implies a connection to poverty reduction by explaining how PV-powered cold chains can benefit smallholder farmers. It cites a report stating that a lack of sustainable cold chains can cut smallholder farmer incomes by about 15%. By providing reliable energy for agriculture and food preservation, PV batteries can help increase incomes and improve livelihoods in rural communities.

2. What specific targets under those SDGs can be identified based on the article’s content?

-

SDG 7: Affordable and Clean Energy

- Target 7.1: By 2030, ensure universal access to affordable, reliable and modern energy services. The article addresses this by discussing rural electrification opportunities, noting that 685 million people lived without electricity in 2022 and highlighting initiatives like “Mission 300” to connect 300 million people in Africa using solutions like solar mini-grids with batteries.

- Target 7.2: By 2030, increase substantially the share of renewable energy in the global energy mix. The article’s core theme supports this target, detailing the rapid expansion of solar PV capacity (407 GW added in 2023) and the corresponding need for battery storage (estimated 1,300 GW required by 2030) to integrate this renewable energy.

-

SDG 2: Zero Hunger

- Target 2.3: By 2030, double the agricultural productivity and incomes of small-scale food producers. The article connects to this by stating that PV-powered cold chains can prevent income losses for smallholder farmers, which are estimated at 15% due to a lack of cold storage.

- Target 2.4: By 2030, ensure sustainable food production systems and implement resilient agricultural practices. The use of solar-powered irrigation and cold storage is presented as a key part of “climate-smart agriculture” and “sustainable cold chains,” which helps reduce food loss and makes food systems more resilient.

-

SDG 13: Climate Action

- Target 13.2: Integrate climate change measures into national policies, strategies and planning. The article mentions government policies like the US Inflation Reduction Act and the EU’s “Fit for 55” package, which provide incentives for solar-plus-storage systems to help meet national emissions reduction goals.

-

SDG 9: Industry, Innovation, and Infrastructure

- Target 9.1: Develop quality, reliable, sustainable and resilient infrastructure. The article describes the build-out of grid-scale battery storage and distributed residential systems as essential infrastructure for a modern, reliable, and renewable-based power grid.

- Target 9.4: By 2030, upgrade infrastructure and retrofit industries to make them sustainable. The massive cost reduction in battery storage (93% between 2010 and 2024) and technological improvements in lithium-ion batteries are examples of retrofitting the energy industry with more efficient and sustainable technologies.

-

SDG 12: Responsible Consumption and Production

- Target 12.3: By 2030, halve per capita global food waste at the retail and consumer levels and reduce food losses along production and supply chains, including post-harvest losses. The article directly addresses this by citing FAO data that 13.3% of food is lost globally after harvest and explaining how PV-powered cold chains can significantly reduce these losses.

- Target 12.5: By 2030, substantially reduce waste generation through prevention, reduction, recycling and reuse. The article highlights this target by discussing the challenge of recycling lithium-ion batteries, noting that less than 20% are currently recycled, and mentioning the EU’s goal to recycle 15% of critical minerals by 2030.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

-

SDG 7: Affordable and Clean Energy

- Indicator 7.1.1 (Proportion of population with access to electricity): The article provides a baseline figure of 685 million people living without electricity in 2022.

- Indicator 7.2.1 (Renewable energy share in total final energy consumption): Progress is shown through data on renewable capacity additions, such as the 407 GW of new solar PV capacity added in 2023, bringing the global total to 1.6 TW.

-

SDG 2: Zero Hunger

- Indicator 12.3.1.a (Food Loss Index): The article explicitly cites the FAO’s SDG data, stating that “13.3% of food is lost globally after harvest at farm, storage, transport and processing stages in 2023.” It also provides specific loss percentages for cereals (20%), dairy/fish (30%), and fruit/vegetables (40%).

- Indicator 2.3.2 (Average income of small-scale food producers): Progress is implied through the statement that sustainable cold chains can prevent a 15% income loss for smallholder farmers.

-

SDG 13: Climate Action

- Indicator 13.2.2 (Total greenhouse gas emissions per year): The article implies this indicator by referencing the EU’s goal to cut emissions by 55% by 2030 and noting that solar irrigation can cut emissions from water pumping by up to 95%.

-

SDG 9: Industry, Innovation, and Infrastructure

- Indicator 9.b.1 (Proportion of medium and high-tech industry value added in total value added): The market size and growth figures for the PV battery market (from USD 7.6 Billion in 2024 to USD 22.6 Billion by 2034) serve as a proxy for the growth of this high-tech, sustainable industry.

-

SDG 12: Responsible Consumption and Production

- Indicator 12.5.1 (National recycling rate, tons of material recycled): The article provides a clear metric by stating that “less than 20% of end-of-life lithium batteries were actually recycled globally as of 2023.” It also mentions the EU’s target to recycle 15% of critical minerals by 2030.

4. Summary Table of SDGs, Targets, and Indicators

| SDGs | Targets | Indicators |

|---|---|---|

| SDG 7: Affordable and Clean Energy |

|

|

| SDG 2: Zero Hunger |

|

|

| SDG 13: Climate Action |

|

|

| SDG 9: Industry, Innovation, and Infrastructure |

|

|

| SDG 12: Responsible Consumption and Production |

|

|

| SDG 1: No Poverty |

|

|

Source: market.us

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0