Hydro Turbine Generator Unit Market Size | CAGR of 7.0% – Market.us

Global Hydro Turbine Generator Unit Market: A Report on Sustainable Energy Infrastructure

Executive Summary

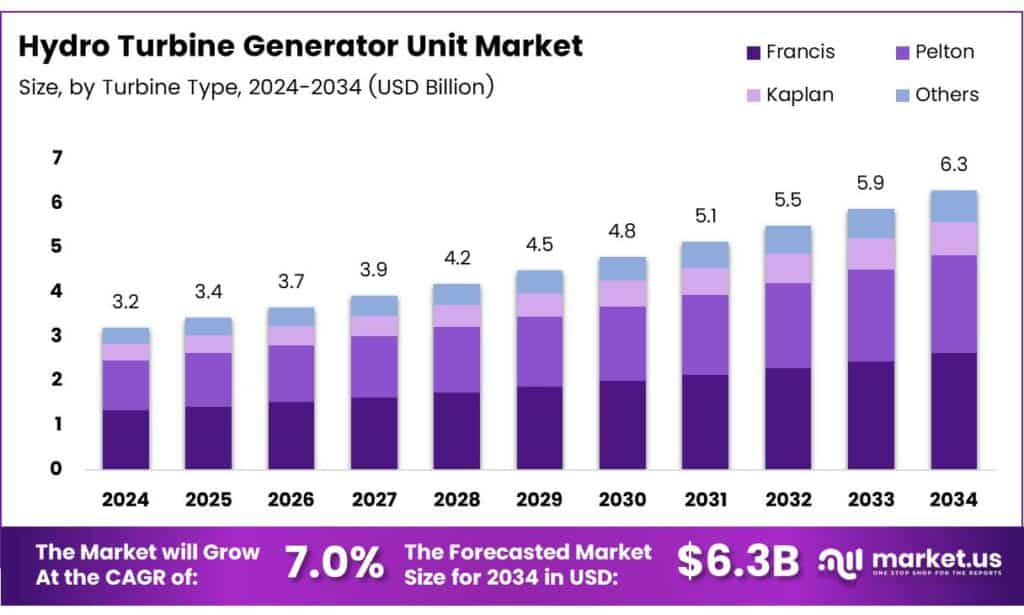

The Global Hydro Turbine Generator Unit Market is integral to the worldwide transition towards sustainable energy, directly supporting the achievement of the United Nations Sustainable Development Goals (SDGs). The market is projected to expand from USD 3.2 billion in 2024 to USD 6.3 billion by 2034, demonstrating a Compound Annual Growth Rate (CAGR) of 7.0%. This growth is propelled by the global imperative to increase the share of renewable energy (SDG 7), combat climate change (SDG 13), and build resilient infrastructure (SDG 9). Hydro turbine generator units, which convert water flow into electricity, are fundamental components of hydropower plants, providing reliable, low-carbon baseload power and essential grid stability services.

Alignment with Sustainable Development Goals (SDGs)

The expansion and modernization of the hydro turbine generator unit market are intrinsically linked to several key SDGs:

- SDG 7: Affordable and Clean Energy: Hydropower is a cornerstone of clean energy systems. The market’s growth directly contributes to increasing the global percentage of renewable energy. Modernization of existing plants enhances efficiency, generating more clean electricity from the same water resources and improving energy access.

- SDG 13: Climate Action: As the third-largest source of global electricity, hydropower displaces fossil fuel generation, significantly reducing greenhouse gas emissions. The projected 230 GW capacity increase by 2030 is a critical step in global climate change mitigation efforts.

- SDG 9: Industry, Innovation, and Infrastructure: The development of new hydropower facilities and the refurbishment of aging ones represent substantial investments in sustainable and resilient infrastructure. Innovations such as digital monitoring and smart turbines enhance operational efficiency and longevity, fostering technological advancement within the energy sector.

- SDG 6 & 15: Clean Water and Life on Land: While a key challenge, modern turbine designs increasingly incorporate features to mitigate environmental impact, such as fish-friendly passage and improved water flow management, aligning with goals for sustainable water management and biodiversity protection.

Market Segmentation Analysis

Turbine Type Analysis

The selection of turbine technology is critical for optimizing energy generation in diverse geographical settings, thereby maximizing contributions to SDG 7.

- Francis Turbines: Dominating the market with a 57.9% share, Francis turbines are highly adaptable for medium-head projects. Their efficiency across varying flow conditions makes them a vital technology for expanding reliable clean energy infrastructure globally.

- Pelton Turbines: Essential for high-head applications, these turbines are crucial for harnessing hydropower potential in mountainous regions, enabling energy generation in challenging terrains and contributing to decentralized energy solutions.

- Kaplan Turbines: Designed for low-head, high-flow environments, Kaplan turbines with their adjustable blades offer operational flexibility. This supports stable power generation from run-of-river plants, minimizing the environmental footprint associated with large reservoirs.

Generator Type Analysis

Generator choice directly impacts grid stability, a crucial factor for integrating intermittent renewables like solar and wind, thus advancing SDG 7.

- Synchronous Generators: Holding a commanding 77.8% market share, synchronous generators are preferred for their ability to maintain a constant speed and frequency. This ensures grid stability and efficient power output, making them indispensable for large-scale hydropower plants that form the backbone of national energy systems.

- Asynchronous Generators: Primarily used in small-scale and micro-hydro projects, these generators support rural electrification and decentralized energy systems. They offer a cost-effective solution for bringing clean energy to remote communities, directly addressing energy access targets within SDG 7.

Head Range Analysis

The operational head range determines the type of hydropower project and its suitability for a given location, influencing the scalability of clean energy deployment.

- Medium Head (100 to 300 meters): This segment leads with a 44.4% share, offering a balanced profile of efficiency and cost-effectiveness. It is the most common project type, significantly contributing to the global portfolio of renewable energy infrastructure.

- Low Head (less than 100 meters): These installations are vital for run-of-river projects, minimizing ecological disruption and supporting power generation in regions with low elevation.

- High Head (above 300 meters): High-head projects maximize energy conversion from limited water flow in steep terrains, unlocking hydropower potential in geographically constrained areas.

Market Dynamics: Drivers and Restraints in the Context of Sustainability

Drivers

The primary driver is the global commitment to the Paris Agreement and the SDGs, which mandates a shift to clean energy sources. Hydropower provides a stable, low-emission solution to meet rising electricity demand. Furthermore, the modernization of aging hydropower plants—with nearly 40% of major facilities requiring upgrades—presents a significant opportunity to enhance the efficiency and output of existing clean energy assets, a key tenet of sustainable infrastructure development (SDG 9).

Restraints

Significant barriers to market expansion include high initial capital investment, which can be prohibitive for developing nations seeking to expand energy access under SDG 7. Moreover, environmental and social concerns related to large dam construction, such as impacts on river ecosystems (SDG 15) and community displacement, necessitate rigorous regulatory processes and sustainable project design, which can extend project timelines.

Emerging Trends

Technological innovation is shaping the market’s future and its alignment with sustainability goals. The adoption of digital monitoring systems and smart turbines enhances operational efficiency and reliability, contributing to SDG 9. Concurrently, a focus on sustainability-by-design, including fish-friendly turbines, demonstrates the industry’s response to environmental regulations and its commitment to protecting biodiversity (SDG 15).

Regional Contribution to Global Energy Goals

North America leads the market with a 45.8% share, valued at USD 1.4 billion. The region’s focus is on refurbishing its extensive existing hydropower infrastructure. These modernization projects enhance the efficiency and lifespan of clean energy assets, reinforcing grid stability and contributing to national climate targets.

Europe is a mature market concentrated on retrofitting existing plants to comply with stringent carbon-reduction goals under the European Green Deal. This strategy maximizes the output of established renewable sources, supporting the continent’s transition to a net-zero economy.

Asia Pacific exhibits strong growth momentum, driven by investments in new hydropower projects to meet the energy demands of rapid urbanization and industrialization. Hydropower is critical for ensuring energy security and balancing the grid as variable renewables like solar and wind are integrated, supporting both economic growth (SDG 8) and clean energy access (SDG 7).

Key Players and Recent Developments

Industry leaders are actively contributing to the global energy transition through technological innovation and strategic projects.

Top Key Players

- General Electric Company

- Siemens Energy AG

- Andritz Hydro GmbH

- Voith Hydro Holding GmbH & Co. KG

- Toshiba Energy Systems & Solutions Corporation

- Harbin Electric Corporation

- Dongfang Electric Corporation

Recent Developments

- 2024: GE Vernova’s contract to supply aerating turbines for the Saluda Hydro plant in the U.S. exemplifies the industry’s focus on modernizing infrastructure to enhance both efficiency and environmental performance.

- 2024: Siemens Energy continues to advance hydropower technology, delivering large variable-speed pumped turbines that enhance grid stability and enable greater integration of other renewable energy sources, directly supporting SDG 7.

1. Which SDGs are addressed or connected to the issues highlighted in the article?

SDG 7: Affordable and Clean Energy

- The article is centered on the hydro turbine generator unit market, which is fundamental to hydropower, a major source of renewable and clean energy. It explicitly states that the market is driven by the “global need for clean and reliable electricity” and the goal to “reduce pollution and dependence on fossil fuels.”

SDG 9: Industry, Innovation, and Infrastructure

- The text discusses the development and modernization of hydropower infrastructure. It highlights “new installations, refurbishment projects, and digital upgrades” and the need to revamp aging plants. The trend towards “Digital Monitoring and Smart Turbines” points directly to innovation within the industry.

SDG 13: Climate Action

- Hydropower is presented as a key tool for climate action. The article describes it as the “backbone of low-carbon electricity” and a “cleaner pathway to offset emissions.” The market’s growth is linked to “compliance with strict carbon-reduction targets.”

SDG 15: Life on Land

- The article acknowledges the environmental impact of hydropower projects, noting that they “may affect river ecosystems, wildlife habitats.” It also points to mitigation efforts, such as turbines “designed to reduce environmental impact by supporting fish-friendly operations and improved water flow control.”

2. What specific targets under those SDGs can be identified based on the article’s content?

SDG 7: Affordable and Clean Energy

- Target 7.2: By 2030, increase substantially the share of renewable energy in the global energy mix. The article directly supports this by detailing the growth of the hydropower market, a key renewable source. It notes that hydropower is the “third largest supplier of global electricity” and projects a “capacity increase of 230 GW by 2030.”

- Target 7.a: By 2030, enhance international cooperation to facilitate access to clean energy research and technology…and promote investment in energy infrastructure and clean energy technology. The article discusses technological advancements like “digital monitoring systems,” “smart turbines,” and “advanced turbine designs,” as well as the global market dynamics involving key international players like General Electric, Siemens Energy, and Andritz Hydro.

SDG 9: Industry, Innovation, and Infrastructure

- Target 9.1: Develop quality, reliable, sustainable and resilient infrastructure…to support economic development and human well-being. The article focuses on hydropower plants, which are critical infrastructure for providing “reliable electricity” and “grid stability.” The discussion on modernizing plants enhances their reliability and sustainability.

- Target 9.4: By 2030, upgrade infrastructure and retrofit industries to make them sustainable, with enhanced resource-use efficiency and greater adoption of clean and environmentally sound technologies. This target is directly addressed in the sections on “Growth Factors” and “Drivers,” which emphasize the “modernization of existing plants” and retrofitting aging turbines to “improve efficiency and lifespan.” The article states that “nearly 40% of major plants aged 45–60 years require revamping.”

SDG 13: Climate Action

- Target 13.2: Integrate climate change measures into national policies, strategies and planning. The article mentions that market growth is driven by government actions, such as “supportive clean-energy policies and federal funding for modernization” in North America and “compliance with strict carbon-reduction targets” in Europe.

SDG 15: Life on Land

- Target 15.1: By 2020, ensure the conservation, restoration and sustainable use of terrestrial and inland freshwater ecosystems and their services. The article touches upon this by acknowledging the environmental concerns of hydro projects on “river ecosystems” and highlighting the industry’s response through “sustainability-focused design” that includes “fish-friendly operations” to mitigate these impacts.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

Indicators for SDG 7 (Affordable and Clean Energy)

- Renewable Energy Capacity: The article provides specific figures that can be used as indicators, such as the “Global installed hydropower capacity reached approximately 1,443 GW” and the projected “capacity increase of 230 GW by 2030.”

- Renewable Energy Generation: The text states that global hydropower generation was about “4,250 TWh,” providing a baseline for measuring progress.

- Investment in Clean Energy: The market size and growth projections serve as a proxy for investment. The market is expected to grow from “USD 3.2 billion in 2024” to “USD 6.3 billion by 2034,” indicating significant ongoing investment in this clean energy technology.

Indicators for SDG 9 (Industry, Innovation, and Infrastructure)

- Infrastructure Modernization Rate: An implied indicator is the scale of modernization efforts. The article quantifies this potential by stating that “nearly 40% of major plants aged 45–60 years require revamping, representing modernization potential of 476 GW.”

- Adoption of New Technologies: The trend of adopting “digital monitoring systems” and “smart turbines” can be tracked as an indicator of innovation and technological upgrading in the sector.

Indicators for SDG 13 (Climate Action)

- Implementation of Climate Policies: The article implies this can be measured by observing market drivers, such as the presence of “supportive clean-energy policies,” “federal funding,” and “carbon-reduction targets” that stimulate the hydro turbine market.

Indicators for SDG 15 (Life on Land)

- Adoption of Environmentally Sound Technology: Progress can be measured by the adoption rate of “sustainability-focused design” in new and refurbished turbines, specifically those with features for “fish-friendly operations and improved water flow control.”

4. SDGs, Targets, and Indicators Table

| SDGs | Targets | Indicators |

|---|---|---|

| SDG 7: Affordable and Clean Energy | 7.2: Increase substantially the share of renewable energy in the global energy mix. |

|

| SDG 9: Industry, Innovation, and Infrastructure | 9.4: Upgrade infrastructure and retrofit industries to make them sustainable. |

|

| SDG 13: Climate Action | 13.2: Integrate climate change measures into national policies, strategies and planning. |

|

| SDG 15: Life on Land | 15.1: Ensure the conservation, restoration and sustainable use of terrestrial and inland freshwater ecosystems. |

|

Source: market.us

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0