Middle East Packaged Wastewater Treatment Market, 2033 – Grand View Research

Report on the Middle East Packaged Wastewater Treatment Market and its Alignment with Sustainable Development Goals

Executive Summary

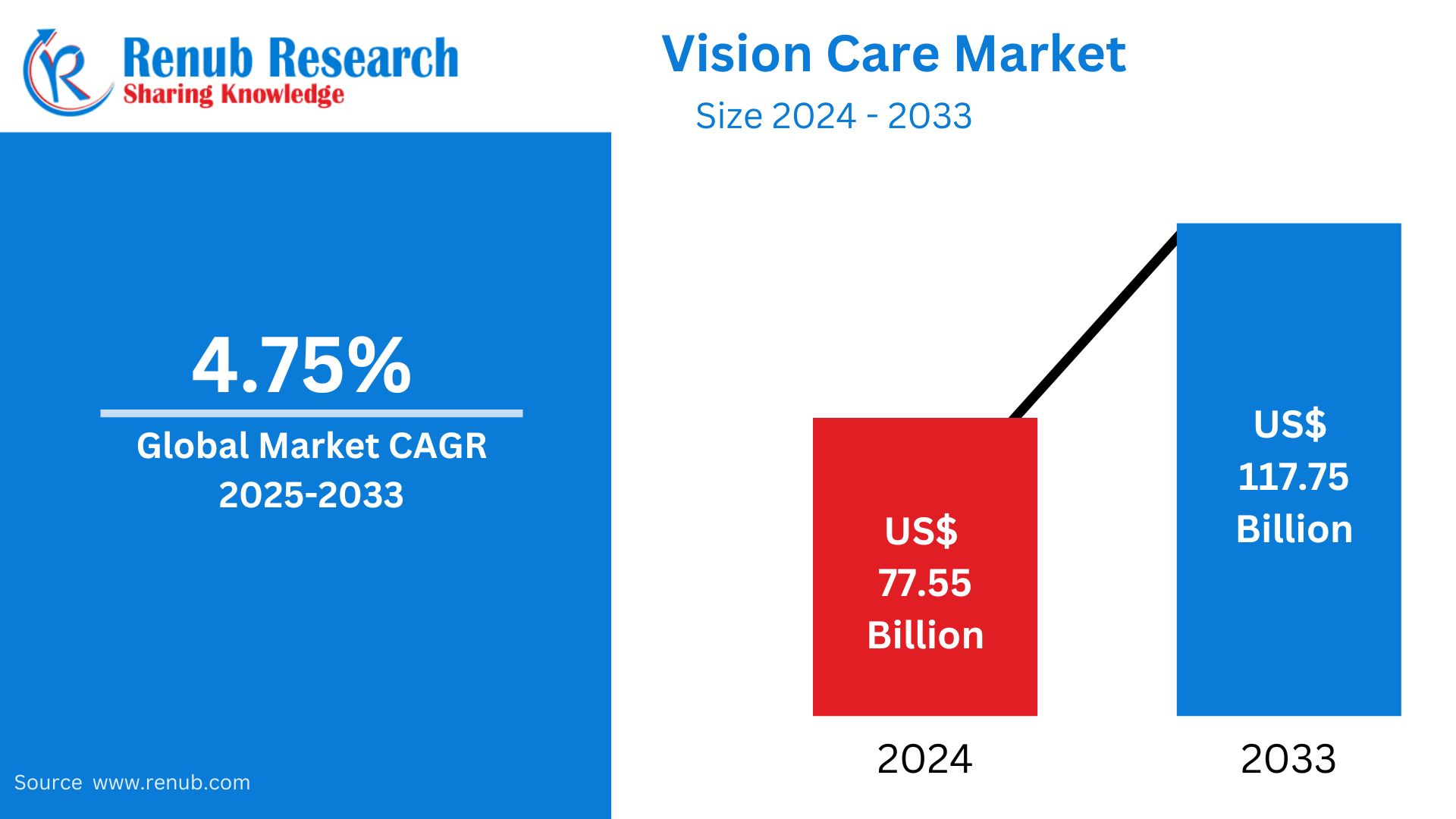

The Middle East packaged wastewater treatment market is poised for significant growth, projected to expand from USD 611.3 million in 2024 to USD 1,339.1 million by 2033, at a Compound Annual Growth Rate (CAGR) of 9.4%. This expansion is fundamentally driven by the region’s urgent need to address severe water scarcity and align with the United Nations’ Sustainable Development Goals (SDGs), particularly SDG 6 (Clean Water and Sanitation). Packaged systems offer decentralized, scalable, and efficient solutions that are critical for achieving sustainable water management in the face of rapid urbanization and industrialization, directly supporting SDG 11 (Sustainable Cities and Communities) and SDG 9 (Industry, Innovation, and Infrastructure).

Market Analysis and SDG Integration

Market Size and Forecast

The market’s robust growth trajectory reflects a regional commitment to building resilient infrastructure and ensuring water security for all. The projected increase underscores the escalating investment in technologies that promote water reuse and recycling, a core target of SDG 6.3.

- 2024 Market Valuation: USD 611.3 Million

- 2033 Market Projection: USD 1,339.1 Million

- Projected CAGR (2025-2033): 9.4%

Market Characteristics and Concentration

The market is characterized by fragmentation, fostering innovation and specialized solutions tailored to diverse regional needs. This competitive landscape accelerates the adoption of advanced technologies, contributing to SDG 9 by fostering innovation in the water sector. Stricter government regulations, aimed at protecting water resources, serve as a primary driver, compelling industries and municipalities to adopt effective treatment solutions in line with SDG 6.3 (improve water quality) and SDG 12 (Responsible Consumption and Production).

Key Market Dynamics

Drivers

- Water Scarcity and SDG 6: Chronic water shortages necessitate efficient wastewater treatment and reuse, making it a cornerstone of national strategies to achieve SDG 6.

- Urbanization and SDG 11: Rapid urban growth demands scalable and decentralized water infrastructure to manage increased wastewater volumes, directly supporting the creation of sustainable cities under SDG 11.

- Industrial Growth and SDG 9 & 12: Expansion in industrial activities requires advanced treatment systems to ensure environmental compliance and promote sustainable industrialization, aligning with the goals of responsible production.

- Government Regulations: Proactive government policies promoting water sustainability and setting stringent discharge standards are crucial for meeting national and international environmental commitments.

Opportunities

- Smart City Integration: The development of smart cities provides a significant opportunity to integrate advanced, IoT-enabled packaged systems, enhancing efficiency and contributing to the goals of SDG 11.

- Technological Advancement: Innovations in treatment technologies offer opportunities to provide more energy-efficient and effective solutions, supporting SDG 13 (Climate Action) by reducing the carbon footprint of water management.

- Expansion to Remote Areas: Deploying containerized and modular systems in underserved rural and remote areas can help achieve universal access to sanitation as mandated by SDG 6.

Segment Analysis in the Context of Sustainability

Technology Insights

The adoption of specific technologies is closely linked to achieving sustainability targets.

- Moving Bed Biofilm Reactor (MBBR): This segment held a 28.2% share in 2024 due to its efficiency and compact design, making it ideal for urban infrastructure projects aligned with SDG 11.

- Membrane Aerated Biofilm Reactor (MABR): Projected to grow at a CAGR of 10.8%, MABR technology is gaining prominence for its significant energy savings. Its efficiency contributes to SDG 12 by reducing resource consumption and supports SDG 13 by lowering greenhouse gas emissions from the water treatment process.

System Type Insights

The choice of system type reflects the need for flexible and resilient infrastructure (SDG 9).

- Modular Treatment Plants: Leading with a 46.4% market share, these systems offer the scalability required for large municipal and industrial projects, facilitating planned urban and industrial development.

- Containerized Systems: With a projected CAGR of 9.9%, these portable and rapidly deployable systems are crucial for providing sanitation in temporary locations, construction sites, and remote communities, ensuring no one is left behind in the pursuit of SDG 6.

End-Use Insights

Wastewater treatment is critical across both municipal and industrial sectors for achieving broad sustainability.

- Municipal Sector: Accounting for 61.0% of the market, this segment is driven by the need to provide sanitation for growing urban populations and protect public health, a foundational aspect of SDG 6 and SDG 11.

- Industrial Sector: As the fastest-growing segment with a projected 10.0% CAGR, its adoption of packaged systems demonstrates a shift towards sustainable industrial practices (SDG 9) and responsible water management (SDG 12) to minimize environmental impact.

Regional and Company Analysis

Country Insights

- Saudi Arabia: Leading the market with a 34.0% share, the Kingdom’s investments under Vision 2030 are directly aligned with achieving SDG 6. The focus on scalable packaged plants supports its rapid economic and urban development goals sustainably.

- United Arab Emirates (UAE): The UAE’s growth is fueled by sustainability initiatives and smart city projects. The adoption of advanced wastewater treatment is integral to its strategy for water reuse, contributing to both SDG 6 and SDG 11.

Key Company Contributions

Leading companies are instrumental in deploying technologies that help the region meet its SDG targets. Firms like Corodex Industries, Emvees Wastewater Treatment LLC, and MENA-Water provide specialized MBR, MBBR, and containerized solutions that enable municipalities and industries to improve water quality, enhance water reuse, and operate more sustainably.

- Corodex Industries CO (L.L.C)

- Emvees Wastewater Treatment LLC

- MENA-Water

- Veolia Environment SA

- Xylem Inc.

- Evoqua Water Technologies LLC

Recent Developments Supporting SDGs

- Dubai Sewerage Fee Adjustment (January 2025): Dubai’s plan to increase sewerage fees is a strategic policy to encourage water conservation (SDG 6.4) and finance the expansion of sustainable wastewater infrastructure, supporting the Dubai 2040 Urban Master Plan and SDG 11.

- Sulzer’s Role in Egypt’s New Delta Plant (July 2024): The supply of over 260 energy-efficient pumps and mixers for the world’s largest treatment plant is a milestone for sustainable water reuse in agriculture. This project directly supports SDG 2 (Zero Hunger) by enhancing food security and SDG 6 by promoting large-scale water recycling.

Analysis of Sustainable Development Goals in the Article

-

Which SDGs are addressed or connected to the issues highlighted in the article?

The article on the Middle East’s packaged wastewater treatment market directly addresses and connects to several Sustainable Development Goals (SDGs) due to its focus on water management, industrial growth, and urban development in a water-scarce region.

- SDG 6: Clean Water and Sanitation: This is the most prominent SDG. The entire article revolves around treating wastewater to address “limited freshwater resources” and “chronic water scarcity,” which is central to ensuring the availability and sustainable management of water and sanitation.

- SDG 9: Industry, Innovation, and Infrastructure: The article highlights the role of “rapid urbanization and industrial growth” in driving demand for wastewater treatment. It discusses technological innovations like MBR, MABR, IoT, and AI, and the development of decentralized infrastructure (packaged systems) to support sustainable industrialization and resilient infrastructure.

- SDG 11: Sustainable Cities and Communities: The text explicitly links the market’s growth to “rapid urbanization” and the needs of expanding urban centers. It notes that the “municipal segment accounted for a share of 61.0% in 2024” and mentions investments in “smart city initiatives,” directly connecting wastewater management to making cities more sustainable and resilient.

- SDG 12: Responsible Consumption and Production: By focusing on treating wastewater for “efficient water reuse,” the article addresses the core of sustainable resource management. This practice reduces the strain on limited freshwater sources, promoting more sustainable consumption patterns for a critical natural resource.

-

What specific targets under those SDGs can be identified based on the article’s content?

Specific targets within the identified SDGs are clearly reflected in the article’s discussion of market drivers, technologies, and applications.

- Target 6.3: “By 2030, improve water quality by reducing pollution… halving the proportion of untreated wastewater and substantially increasing recycling and safe reuse globally.” The article’s central theme is the expansion of wastewater treatment capabilities to “ensure safe water reuse” and meet “stringent environmental regulations,” which directly aligns with this target.

- Target 6.4: “By 2030, substantially increase water-use efficiency across all sectors and ensure sustainable withdrawals and supply of freshwater to address water scarcity.” The market is driven by the need to “enable efficient water reuse” in response to the “Middle East’s chronic water scarcity,” which is the essence of this target.

- Target 9.4: “By 2030, upgrade infrastructure and retrofit industries to make them sustainable, with increased resource-use efficiency and greater adoption of clean and environmentally sound technologies…” The article details the adoption of “advanced technologies such as MBBR, MBR, and RO” and the integration of “IoT and AI to monitor systems and optimize performance” in both municipal and industrial sectors, reflecting this target’s goal.

- Target 11.6: “By 2030, reduce the adverse per capita environmental impact of cities, including by paying special attention to… municipal and other waste management.” The article’s focus on the large and growing “municipal segment” for wastewater treatment in response to “growing urban populations” directly addresses the challenge of managing waste in cities.

- Target 12.2: “By 2030, achieve the sustainable management and efficient use of natural resources.” The entire industry described in the article is a mechanism for achieving more sustainable and efficient use of water, a critical natural resource, especially in the arid Middle East.

-

Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

The article, being a market analysis report, is rich with quantitative and qualitative data that can serve as indicators for measuring progress towards these SDG targets.

- Indicator for Target 6.3: The growth of the wastewater treatment market itself serves as a proxy indicator for the proportion of wastewater treated. The market size, projected to grow from USD 611.3 million in 2024 to USD 1,339.1 million by 2033, indicates a substantial increase in investment and capacity for wastewater treatment and reuse.

- Indicator for Target 9.4: The rate of adoption of advanced and efficient technologies is a clear indicator. The article provides specific metrics, such as the projected Compound Annual Growth Rate (CAGR) of 10.8% for the Membrane Aerated Biofilm Reactor (MABR) segment and the 10.0% CAGR for the industrial end-use segment, showing a clear trend towards adopting cleaner and more efficient industrial processes.

- Indicator for Target 11.6: The market share of the municipal wastewater treatment segment is a direct indicator of urban waste management efforts. The article states that the municipal segment accounted for a 61.0% share in 2024, providing a baseline to measure progress in managing wastewater from growing urban populations.

- Indicator for Target 6.4 & 12.2: The overall market growth rate (CAGR of 9.4%) is an indicator of the increasing emphasis on water-use efficiency and sustainable resource management. The expansion of this market is directly driven by the need to reuse water to combat scarcity, making its financial growth a measure of the scale of these efforts.

SDG Analysis Summary Table

| SDGs | Targets | Indicators |

|---|---|---|

| SDG 6: Clean Water and Sanitation | Target 6.3: Improve water quality by increasing wastewater treatment and safe reuse. | Projected market growth from USD 611.3 million (2024) to USD 1,339.1 million (2033), indicating increased capacity for treating wastewater. |

| SDG 9: Industry, Innovation, and Infrastructure | Target 9.4: Upgrade infrastructure and industries with sustainable and clean technologies. | Expected CAGR of 10.8% for the advanced MABR technology segment and 10.0% for the industrial segment, showing adoption of efficient technologies. |

| SDG 11: Sustainable Cities and Communities | Target 11.6: Reduce the environmental impact of cities through improved waste management. | The municipal segment’s market share of 61.0% in 2024, reflecting the scale of urban wastewater management efforts. |

| SDG 12: Responsible Consumption and Production | Target 12.2: Achieve sustainable management and efficient use of natural resources. | The overall market CAGR of 9.4%, driven by the need for “efficient water reuse” to address “chronic water scarcity.” |

Source: grandviewresearch.com

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0