Smart Power Distribution Systems Market to Hit US$ 118.4 Billion by 2035, Growing at 8.9% CAGR – openPR.com

Report on the Global Smart Power Distribution Systems Market and its Contribution to Sustainable Development Goals

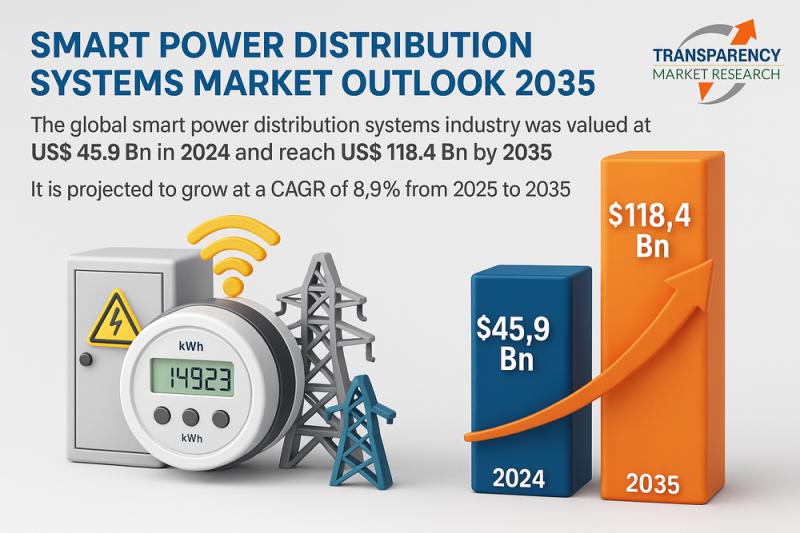

1.0 Market Overview and Projections

The global market for Smart Power Distribution Systems (SPDS) was valued at USD 45.9 billion in 2024. It is projected to experience significant growth, reaching an estimated USD 118.4 billion by 2035, which corresponds to a Compound Annual Growth Rate (CAGR) of 8.9% from 2025 to 2035. This expansion is fundamentally linked to global efforts to achieve key Sustainable Development Goals (SDGs), particularly those concerning energy, infrastructure, and sustainable cities. The growth is propelled by investments in smart grid infrastructure, rising electricity demand, and the adoption of digital technologies that enhance energy efficiency and grid reliability, directly supporting the transition to a more sustainable global energy landscape.

2.0 Alignment with Sustainable Development Goals (SDGs)

The development and deployment of Smart Power Distribution Systems are critical enablers for achieving several United Nations Sustainable Development Goals. The market’s growth is intrinsically tied to the global sustainability agenda.

- SDG 7 (Affordable and Clean Energy): SPDS are essential for integrating variable renewable energy sources like solar and wind into the grid. By improving efficiency, reducing energy losses, and enabling better load management, these systems contribute to making energy more reliable, sustainable, and affordable for all.

- SDG 9 (Industry, Innovation, and Infrastructure): The modernization of legacy power grids with smart technology represents a significant upgrade to critical infrastructure. This fosters innovation in energy management and builds resilient systems capable of withstanding disruptions, which is a core target of SDG 9.

- SDG 11 (Sustainable Cities and Communities): As urbanization accelerates, SPDS provide the backbone for smart cities, ensuring a reliable and efficient electricity supply for dense populations and critical urban services. This supports the development of inclusive, safe, resilient, and sustainable urban environments.

- SDG 13 (Climate Action): By enabling a higher penetration of renewable energy and optimizing energy consumption, SPDS directly contribute to the reduction of greenhouse gas emissions from the power sector, playing a vital role in climate change mitigation efforts.

3.0 Market Segmentation Analysis

The market is segmented based on component, solution, application, and end-use industry, with each segment contributing to sustainability objectives.

-

By Component

- Hardware: Includes smart meters, sensors, controllers, and circuit monitors. The widespread deployment of this hardware is foundational for achieving SDG 7 by providing the data necessary for consumers and utilities to manage energy consumption effectively.

- Software: Encompasses analytics platforms, grid monitoring software, and energy management systems. This segment is poised for rapid growth, driving innovation (SDG 9) through AI and machine learning for predictive maintenance and grid optimization.

- Services: Consists of consulting, integration, support, and maintenance. These services ensure the effective deployment and operation of resilient infrastructure (SDG 9).

-

By Solution

- Advanced Metering Infrastructure (AMI): A dominant solution that facilitates two-way communication, providing real-time data crucial for efficient energy management and supporting SDG 7.

- Distribution Automation (DA): Growing significantly, DA enhances grid reliability and optimizes fault management, contributing to the resilient infrastructure goals of SDG 9 and SDG 11.

- Other Solutions: Grid Asset Management, Smart Grid Communication, and Substation Automation further enhance the grid’s efficiency and resilience.

-

By Application

The Distribution segment holds the largest market share, as SPDS are primarily focused on improving the final delivery of electricity, which is critical for ensuring universal access to reliable energy (SDG 7).

-

By End-Use Industry

- Energy and Utilities: The primary adopters, investing in modernization to meet regulatory requirements and sustainability targets.

- Residential and Commercial: These sectors drive demand for smart meters and energy management systems to reduce costs and environmental impact, aligning with SDG 11 and SDG 13.

4.0 Regional Analysis and SDG Impact

- North America: Leads the market due to significant investments in smart grid technologies to modernize aging infrastructure (SDG 9) and enhance energy reliability.

- Asia-Pacific (APAC): Projected to be the fastest-growing region. This growth is driven by rapid urbanization and industrialization (SDG 11), with governments in China, India, and South Korea investing heavily in grid automation to meet rising energy demands sustainably.

- Europe: A strong market driven by regulatory frameworks like the European Green Deal, which promotes decarbonization and the integration of renewable energy, directly aligning with SDG 7 and SDG 13.

5.0 Market Drivers and Challenges

5.1 Drivers

- Integration of Renewable Energy: SPDS are essential for managing the variability of solar and wind power, enabling the clean energy transition as mandated by SDG 7.

- Modernization of Aging Infrastructure: Upgrading legacy grids is crucial for building the resilient infrastructure required by SDG 9 and preventing outages in sustainable cities (SDG 11).

- Rapid Urbanization and Industrialization: Growing energy demand from expanding urban centers necessitates more efficient and resilient power delivery systems to support sustainable development.

- Operational Cost Reduction: Smart systems reduce energy losses and operational expenditures, contributing to the ‘affordable’ aspect of SDG 7.

5.2 Challenges

- High Initial Capital Investment: The cost of deployment can be a barrier to upgrading infrastructure (SDG 9), particularly in developing economies.

- Cybersecurity Threats: The increasing digitization of the grid creates vulnerabilities, making robust security essential for protecting the critical infrastructure targeted by SDG 9 and SDG 11.

- Technical Integration Complexity: Merging modern technologies with legacy systems presents technical challenges to achieving widespread grid modernization.

6.0 Future Outlook and Technological Trends

The market’s future is defined by deeper technological integration aimed at creating autonomous, resilient, and sustainable energy systems.

- Artificial Intelligence (AI) and Machine Learning: AI-driven analytics will enable predictive fault detection and autonomous grid reconfiguration, creating self-healing grids that advance the resilience goals of SDG 9 and SDG 11.

- Distributed Energy Resources (DERs) and Microgrids: SPDS will be crucial for managing decentralized energy sources like rooftop solar and battery storage, fostering local energy independence and supporting the clean energy objectives of SDG 7.

- Electrification of Transport: The growth of electric vehicles (EVs) requires smart load management capabilities to ensure grid stability, directly linking SPDS to the decarbonization of transport under SDG 13.

7.0 Competitive Landscape

The market is competitive, with key players focusing on innovation and strategic partnerships to advance grid modernization. Leading companies include Siemens AG, Schneider Electric, ABB Ltd., Eaton Corporation, and General Electric (GE). Recent developments focus on launching AI-powered software for grid optimization and forming partnerships with utilities to accelerate national grid modernization projects, thereby fast-tracking progress towards global sustainability targets.

Analysis of Sustainable Development Goals in the Article

1. Which SDGs are addressed or connected to the issues highlighted in the article?

-

SDG 7: Affordable and Clean Energy

- The article focuses on Smart Power Distribution Systems (SPDS) which are crucial for ensuring a reliable, efficient, and modern energy supply. It discusses enhancing “grid reliability,” improving “energy efficiency,” and integrating “renewable energy sources” like solar and wind, all of which are central to SDG 7.

-

SDG 9: Industry, Innovation, and Infrastructure

- The core theme is the modernization of energy infrastructure. The article highlights the need to upgrade “decades-old, legacy power grids” and invest in “smart grid technologies,” “advanced automation,” and “digital monitoring.” This directly relates to building resilient infrastructure and fostering innovation.

-

SDG 11: Sustainable Cities and Communities

- The article links the growth of the SPDS market to “rapid urbanization and industrialization.” It emphasizes the need for “resilient and efficient power delivery” in expanding “urban centers,” which is a key component of making cities sustainable and resilient.

-

SDG 13: Climate Action

- The article explicitly states that SPDS are essential for managing renewable energy sources to create a stable grid. It also mentions that regulations like the “European Green Deal” promote “decarbonization,” directly connecting the technology to climate change mitigation efforts.

2. What specific targets under those SDGs can be identified based on the article’s content?

-

Under SDG 7 (Affordable and Clean Energy):

- Target 7.1: Ensure universal access to affordable, reliable and modern energy services. The article’s emphasis on creating an “uninterrupted electricity supply” and improving “grid reliability” directly supports this target.

- Target 7.2: Increase substantially the share of renewable energy in the global energy mix. The text identifies the “Integration of Renewable Energy Sources” like “solar and wind power” as a primary market driver for SPDS.

- Target 7.3: Double the global rate of improvement in energy efficiency. The article repeatedly mentions that these systems “enhance energy efficiency” and enable “optimized load balancing, significantly reducing energy losses.”

-

Under SDG 9 (Industry, Innovation, and Infrastructure):

- Target 9.1: Develop quality, reliable, sustainable and resilient infrastructure. The entire article is about modernizing power infrastructure to be more “efficient, reliable, and resilient.”

- Target 9.4: Upgrade infrastructure and retrofit industries to make them sustainable. The discussion on “Aging Infrastructure Modernization” and the adoption of “advanced automation and digital monitoring technologies” aligns with this target of upgrading infrastructure with cleaner and more efficient technology.

-

Under SDG 11 (Sustainable Cities and Communities):

- Target 11.b: By 2020, substantially increase the number of cities and human settlements adopting and implementing integrated policies and plans towards… resilience to disasters. The article describes how SPDS enhance the “resilience of the local electricity delivery network,” which is a critical service for urban resilience.

-

Under SDG 13 (Climate Action):

- Target 13.2: Integrate climate change measures into national policies, strategies and planning. The mention of the “European Green Deal” as a driver for SPDS adoption through its focus on “decarbonization” is a direct example of this target in action.

3. Are there any indicators mentioned or implied in the article that can be used to measure progress towards the identified targets?

-

Implied Indicators for SDG 7:

- Reliability of electricity supply: The article’s focus on preventing “outages” and ensuring “uninterrupted electricity supply” implies indicators such as the frequency and duration of power interruptions (SAIDI/SAIFI).

- Share of renewable energy: The discussion on integrating “solar and wind power” implies the need to measure the percentage of renewable energy in the total energy consumption.

- Energy efficiency improvements: The goal of “reducing energy losses” implies an indicator related to the reduction in transmission and distribution losses as a percentage of total power generated.

-

Implied Indicators for SDG 9:

- Investment in infrastructure: The article highlights “increasing investments in smart grids” and “heavy government investment in grid automation.” This suggests that investment in sustainable and resilient infrastructure (as a percentage of GDP) could be a relevant indicator.

- Adoption of advanced technology: The growth of the market for “smart meters,” “sensors,” and “grid monitoring software” can serve as a proxy indicator for the adoption of modern and clean technologies.

-

Implied Indicators for SDG 11:

- Access to reliable services in urban areas: The need for “resilient and efficient power delivery” in “urban centers” implies an indicator measuring the proportion of the urban population with a reliable and modern electricity supply.

-

Implied Indicators for SDG 13:

- Reduction in greenhouse gas emissions: The mention of “decarbonization” as a policy driver implies that a key indicator is the reduction of CO2 emissions from the energy sector, facilitated by improved efficiency and higher renewable energy integration.

4. Summary Table of SDGs, Targets, and Indicators

| SDGs | Targets | Indicators (Implied from the Article) |

|---|---|---|

| SDG 7: Affordable and Clean Energy |

7.1: Ensure universal access to reliable and modern energy services. 7.2: Increase the share of renewable energy. 7.3: Double the rate of improvement in energy efficiency. |

– Frequency and duration of power outages. – Percentage share of renewable energy (solar, wind) in the grid. – Reduction in transmission and distribution energy losses. |

| SDG 9: Industry, Innovation, and Infrastructure |

9.1: Develop quality, reliable, sustainable and resilient infrastructure. 9.4: Upgrade infrastructure with clean and environmentally sound technologies. |

– Level of investment in smart grid modernization. – Rate of adoption of smart meters, sensors, and automation software. |

| SDG 11: Sustainable Cities and Communities | 11.b: Implement integrated policies for resilience. | – Percentage of urban population with access to a resilient and reliable electricity supply. |

| SDG 13: Climate Action | 13.2: Integrate climate change measures into national policies. | – Reduction of greenhouse gas emissions from the energy sector due to efficiency and renewables (decarbonization). |

Source: openpr.com

What is Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0